Basic Functionality

Contents

5.2. Basic Functionality#

5.2.1. Industry portfolios data#

In this lecture, we will use industry portfolio data by industry at a monthly frequency.

those are portfolio of stocks of firms in different sectors of the economy

import pandas as pd

%matplotlib inline

First, we will download the data directly from a url and read it into a pandas DataFrame.

## Load up the data -- this will take a couple seconds

url = "https://raw.githubusercontent.com/amoreira2/Lectures/main/assets/data/49_Industry_Portfolios.CSV"

industret_raw = pd.read_csv(url, parse_dates=["Date"])

The pandas read_csv will determine most datatypes of the underlying columns. The

exception here is that we need to give pandas a hint so it can load up the Date column as a Python datetime type: the parse_dates=["Date"].

We can see the basic structure of the downloaded data by getting the first 5 rows, which directly matches the underlying CSV file.

industret_raw.head()

| Date | industry | returns | nfirms | size | |

|---|---|---|---|---|---|

| 0 | 1926-07-31 | Agric | 2.37 | 3 | 99.80 |

| 1 | 1926-07-31 | Food | 0.12 | 40 | 31.19 |

| 2 | 1926-07-31 | Soda | -99.99 | 0 | -99.99 |

| 3 | 1926-07-31 | Beer | -5.19 | 3 | 7.12 |

| 4 | 1926-07-31 | Smoke | 1.29 | 16 | 59.72 |

Note that a row has a date, industry , returns, number of firms in the portfolio and average size of the firm.

Note also the -99.99 which in this case is code for missing observation

For our analysis, we want to look at the firm size across different industries over time, which requires a transformation of the data similar to an Excel pivot-table.

# Don't worry about the details here quite yet

size_all = (

industret_raw

.reset_index()

.pivot_table(index="Date", columns="industry", values="size")

)

size_all.head()

| industry | Aero | Agric | Autos | Banks | Beer | BldMt | Books | Boxes | BusSv | Chems | ... | Smoke | Soda | Softw | Steel | Telcm | Toys | Trans | Txtls | Util | Whlsl |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||||

| 1926-07-31 | 9.52 | 99.80 | 47.55 | 14.50 | 7.12 | 20.80 | 4.33 | 35.35 | 11.21 | 57.59 | ... | 59.72 | -99.99 | -99.99 | 48.56 | 350.36 | 13.00 | 68.67 | 5.78 | 81.22 | 1.19 |

| 1926-08-31 | 9.46 | 102.06 | 55.11 | 15.17 | 6.75 | 21.30 | 6.50 | 37.86 | 11.81 | 62.13 | ... | 60.47 | -99.99 | -99.99 | 50.39 | 353.27 | 14.12 | 69.79 | 5.79 | 86.81 | 0.90 |

| 1926-09-30 | 8.78 | 104.34 | 57.11 | 16.97 | 8.58 | 22.27 | 9.29 | 36.82 | 11.99 | 65.53 | ... | 64.03 | -99.99 | -99.99 | 51.21 | 360.96 | 16.50 | 72.90 | 6.25 | 85.01 | 0.95 |

| 1926-10-31 | 8.15 | 102.91 | 59.69 | 16.46 | 8.92 | 22.04 | 8.83 | 34.77 | 12.01 | 68.47 | ... | 64.42 | -99.99 | -99.99 | 51.02 | 364.16 | 17.88 | 72.71 | 6.36 | 86.41 | 0.88 |

| 1926-11-30 | 7.07 | 102.34 | 54.81 | 14.52 | 8.62 | 21.05 | 9.31 | 32.80 | 12.17 | 65.06 | ... | 65.08 | -99.99 | -99.99 | 48.90 | 363.74 | 17.62 | 70.58 | 6.38 | 83.92 | 0.74 |

5 rows × 49 columns

size_all.columns

Index(['Aero ', 'Agric', 'Autos', 'Banks', 'Beer ', 'BldMt', 'Books', 'Boxes',

'BusSv', 'Chems', 'Chips', 'Clths', 'Cnstr', 'Coal ', 'Drugs', 'ElcEq',

'FabPr', 'Fin ', 'Food ', 'Fun ', 'Gold ', 'Guns ', 'Hardw', 'Hlth ',

'Hshld', 'Insur', 'LabEq', 'Mach ', 'Meals', 'MedEq', 'Mines', 'Oil ',

'Other', 'Paper', 'PerSv', 'RlEst', 'Rtail', 'Rubbr', 'Ships', 'Smoke',

'Soda ', 'Softw', 'Steel', 'Telcm', 'Toys ', 'Trans', 'Txtls', 'Util ',

'Whlsl'],

dtype='object', name='industry')

Finally, we can filter it to look at a subset of the columns (i.e. “industry” in this case).

industries = [

"Autos","Banks", "Meals", "Softw",

"Smoke", "Telcm", "Mines"

]

size = size_all[industries]

size.tail()

| industry | Autos | Banks | Meals | Softw | Smoke | Telcm | Mines |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 2020-11-30 | 11504.82 | 5372.76 | 8638.65 | 22509.62 | 59424.37 | 20127.11 | 7379.30 |

| 2020-12-31 | 15667.02 | 6344.33 | 9595.61 | 24701.31 | 64210.14 | 23242.82 | 8377.75 |

| 2021-01-31 | 18292.42 | 6813.01 | 9983.06 | 25503.86 | 68622.27 | 24468.39 | 9186.89 |

| 2021-02-28 | 20561.46 | 6581.58 | 9531.13 | 25834.04 | 67059.98 | 23911.24 | 9376.07 |

| 2021-03-31 | 18531.08 | 7511.02 | 10445.51 | 26799.04 | 70900.88 | 24972.99 | 10770.47 |

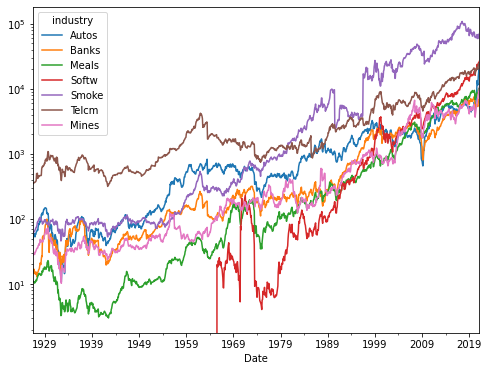

When plotting, a DataFrame knows the column and index names.

size.plot(figsize=(8, 6),logy=True)

<AxesSubplot:xlabel='Date'>

See exercise 1 in the exercise list

5.2.2. Dates in pandas#

You might have noticed that our index now has a nice format for the

dates (YYYY-MM-DD) rather than just a year.

This is because the dtype of the index is a variant of datetime.

size.index

DatetimeIndex(['1926-07-31', '1926-08-31', '1926-09-30', '1926-10-31',

'1926-11-30', '1926-12-31', '1927-01-31', '1927-02-28',

'1927-03-31', '1927-04-30',

...

'2020-06-30', '2020-07-31', '2020-08-31', '2020-09-30',

'2020-10-31', '2020-11-30', '2020-12-31', '2021-01-31',

'2021-02-28', '2021-03-31'],

dtype='datetime64[ns]', name='Date', length=1137, freq=None)

We can index into a DataFrame with a DatetimeIndex using string

representations of dates.

For example

# Data corresponding to a single date

size.loc["01/31/2000", :]

industry

Autos 2461.97

Banks 2249.50

Meals 800.97

Softw 3597.20

Smoke 12584.58

Telcm 8978.29

Mines 967.26

Name: 2000-01-31 00:00:00, dtype: float64

# Data for all days between New Years Day and June first in the year 2000

size.loc["01/31/2000":"06/30/2000", :]

| industry | Autos | Banks | Meals | Softw | Smoke | Telcm | Mines |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 2000-01-31 | 2461.97 | 2249.50 | 800.97 | 3597.20 | 12584.58 | 8978.29 | 967.26 |

| 2000-02-29 | 2504.11 | 2203.67 | 741.71 | 3270.95 | 11499.46 | 8739.86 | 955.71 |

| 2000-03-31 | 2290.96 | 1974.93 | 652.38 | 3603.68 | 11038.70 | 8463.58 | 881.00 |

| 2000-04-30 | 2545.41 | 2291.46 | 767.18 | 3733.34 | 11335.75 | 9098.77 | 938.08 |

| 2000-05-31 | 2873.71 | 2225.48 | 796.35 | 3050.85 | 14605.66 | 8217.91 | 865.02 |

| 2000-06-30 | 2458.02 | 2414.05 | 762.56 | 2740.98 | 17434.72 | 7235.48 | 871.13 |

We will learn more about what pandas can do with dates and times in an upcoming lecture on time series data.

5.2.3. DataFrame Aggregations#

Let’s talk about aggregations.

Loosely speaking, an aggregation is an operation that combines multiple values into a single value.

For example, computing the mean of three numbers (for example

[0, 1, 2]) returns a single number (1).

We will use aggregations extensively as we analyze and manipulate our data.

Thankfully, pandas makes this easy!

5.2.3.1. Built-in Aggregations#

pandas already has some of the most frequently used aggregations.

For example:

Mean (

mean)Variance (

var)Standard deviation (

std)Minimum (

min)Median (

median)Maximum (

max)etc…

Note

When looking for common operations, using “tab completion” goes a long way.

size.mean()

industry

Autos 1271.677274

Banks 952.728619

Meals 984.425286

Softw 1550.233544

Smoke 12058.789384

Telcm 3468.995172

Mines 970.964626

dtype: float64

As seen above, the aggregation’s default is to aggregate each column.

However, by using the axis keyword argument, you can do aggregations by

row as well.

size.var(axis=1).head()

Date

1926-07-31 19263.014148

1926-08-31 19496.461081

1926-09-30 20222.654548

1926-10-31 20548.252614

1926-11-30 20565.567314

dtype: float64

Note that below min and max are not in quotes becasue these are functions defined in python enviroment, while mean and std are in quotes because they are methods of the dataframe.

min and max are objects that python understand in general, while mean and std it only understands in the context of the dataframe.

size.agg([min, max,'mean','std'])

| Autos | Banks | Meals | Softw | Smoke | Telcm | Mines | |

|---|---|---|---|---|---|---|---|

| min | 10.790000 | 13.000000 | 3.010000 | -99.990000 | 45.980000 | 317.100000 | 10.270000 |

| max | 20561.460000 | 7548.840000 | 10445.510000 | 26799.040000 | 109069.340000 | 24972.990000 | 10770.470000 |

| mean | 1271.677274 | 952.728619 | 984.425286 | 1550.233544 | 12058.789384 | 3468.995172 | 970.964626 |

| std | 1899.907582 | 1566.005467 | 2027.328596 | 3831.668701 | 22297.623981 | 4569.770894 | 1702.291519 |

5.2.4. Transforms#

Many analytical operations do not necessarily involve an aggregation.

The output of a function applied to a Series might need to be a new Series.

Some examples:

Compute the percentage change in average firm size from month to month.

Calculate the cumulative sum of elements in each column.

5.2.4.1. Built-in Transforms#

pandas comes with many transform functions including:

Cumulative sum/max/min/product (

cum(sum|min|max|prod))Difference (

diff)Elementwise addition/subtraction/multiplication/division (

+,-,*,/)Percent change (

pct_change)Number of occurrences of each distinct value (

value_counts)Absolute value (

abs)

Again, tab completion is helpful when trying to find these functions.

size.head()

| industry | Autos | Banks | Meals | Softw | Smoke | Telcm | Mines |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 1926-07-31 | 47.55 | 14.50 | 10.82 | -99.99 | 59.72 | 350.36 | 27.74 |

| 1926-08-31 | 55.11 | 15.17 | 11.00 | -99.99 | 60.47 | 353.27 | 29.30 |

| 1926-09-30 | 57.11 | 16.97 | 10.94 | -99.99 | 64.03 | 360.96 | 29.45 |

| 1926-10-31 | 59.69 | 16.46 | 10.80 | -99.99 | 64.42 | 364.16 | 29.46 |

| 1926-11-30 | 54.81 | 14.52 | 10.33 | -99.99 | 65.08 | 363.74 | 28.51 |

size.pct_change().head()

| industry | Autos | Banks | Meals | Softw | Smoke | Telcm | Mines |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 1926-07-31 | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 1926-08-31 | 0.158991 | 0.046207 | 0.016636 | 0.0 | 0.012559 | 0.008306 | 0.056236 |

| 1926-09-30 | 0.036291 | 0.118655 | -0.005455 | 0.0 | 0.058872 | 0.021768 | 0.005119 |

| 1926-10-31 | 0.045176 | -0.030053 | -0.012797 | 0.0 | 0.006091 | 0.008865 | 0.000340 |

| 1926-11-30 | -0.081756 | -0.117861 | -0.043519 | 0.0 | 0.010245 | -0.001153 | -0.032247 |

size.diff().head()

| industry | Autos | Banks | Meals | Softw | Smoke | Telcm | Mines |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 1926-07-31 | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 1926-08-31 | 7.56 | 0.67 | 0.18 | 0.0 | 0.75 | 2.91 | 1.56 |

| 1926-09-30 | 2.00 | 1.80 | -0.06 | 0.0 | 3.56 | 7.69 | 0.15 |

| 1926-10-31 | 2.58 | -0.51 | -0.14 | 0.0 | 0.39 | 3.20 | 0.01 |

| 1926-11-30 | -4.88 | -1.94 | -0.47 | 0.0 | 0.66 | -0.42 | -0.95 |

Transforms can be split into to several main categories:

Series transforms: functions that take in one Series and produce another Series. The index of the input and output does not need to be the same.

Scalar transforms: functions that take a single value and produce a single value. An example is the

absmethod, or adding a constant to each value of a Series.

5.2.4.2. Custom Series Transforms#

pandas also simplifies applying custom Series transforms to a Series or the columns of a DataFrame. The steps are:

Write a Python function that takes a Series and outputs a new Series.

Pass our new function as an argument to the

applymethod (alternatively, thetransformmethod).

As an example, we will standardize our return data to have mean 0 and standard deviation 1.

After doing this, we can use an aggregation to determine at which date the return is most different from “normal times” for each industry.

# lets now work with the return data

returns_all = (

industret_raw

.reset_index()

.pivot_table(index="Date", columns="industry", values="returns")

)

returns = returns_all[industries]

returns.head()

| industry | Autos | Banks | Meals | Softw | Smoke | Telcm | Mines |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 1926-07-31 | 16.39 | 4.61 | 1.87 | -99.99 | 1.29 | 0.83 | 5.64 |

| 1926-08-31 | 4.23 | 11.83 | -0.13 | -99.99 | 6.50 | 2.17 | 0.55 |

| 1926-09-30 | 4.83 | -1.75 | -0.56 | -99.99 | 1.26 | 2.41 | 1.74 |

| 1926-10-31 | -7.93 | -11.82 | -4.11 | -99.99 | 1.06 | -0.11 | -3.20 |

| 1926-11-30 | -0.66 | -2.97 | 4.33 | -99.99 | 4.55 | 1.63 | 8.46 |

#

# Step 1: We write the Series transform function that we'd like to use

#

def standardize_data(x):

"""

Changes the data in a Series to become mean 0 with standard deviation 1

"""

mu = x.mean()

std = x.std()

return (x - mu)/std

#

# Step 2: Apply our function via the apply method.

#

std_returns = returns.apply(standardize_data)

std_returns.head()

| industry | Autos | Banks | Meals | Softw | Smoke | Telcm | Mines |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 1926-07-31 | 1.849843 | 0.488467 | 0.121700 | -1.177902 | 0.025602 | -0.007572 | 0.632371 |

| 1926-08-31 | 0.370785 | 1.512875 | -0.186634 | -1.177902 | 0.920361 | 0.283083 | -0.066595 |

| 1926-09-30 | 0.443765 | -0.413921 | -0.252926 | -1.177902 | 0.020450 | 0.335140 | 0.096817 |

| 1926-10-31 | -1.108273 | -1.842701 | -0.800219 | -1.177902 | -0.013898 | -0.211464 | -0.581551 |

| 1926-11-30 | -0.224001 | -0.587020 | 0.500951 | -1.177902 | 0.585470 | 0.165953 | 1.019618 |

# Takes the absolute value of all elements of a function

abs_std_returns = std_returns.abs()

abs_std_returns.head()

| industry | Autos | Banks | Meals | Softw | Smoke | Telcm | Mines |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 1926-07-31 | 1.849843 | 0.488467 | 0.121700 | 1.177902 | 0.025602 | 0.007572 | 0.632371 |

| 1926-08-31 | 0.370785 | 1.512875 | 0.186634 | 1.177902 | 0.920361 | 0.283083 | 0.066595 |

| 1926-09-30 | 0.443765 | 0.413921 | 0.252926 | 1.177902 | 0.020450 | 0.335140 | 0.096817 |

| 1926-10-31 | 1.108273 | 1.842701 | 0.800219 | 1.177902 | 0.013898 | 0.211464 | 0.581551 |

| 1926-11-30 | 0.224001 | 0.587020 | 0.500951 | 1.177902 | 0.585470 | 0.165953 | 1.019618 |

# find the date when returns was "most different from normal" for each industry

def idxmax(x):

# idxmax of Series will return index of maximal value

return x.idxmax()

abs_std_returns.agg(idxmax)

industry

Autos 1933-04-30

Banks 1933-04-30

Meals 1973-11-30

Softw 1970-09-30

Smoke 1933-04-30

Telcm 1932-08-31

Mines 1932-07-31

dtype: datetime64[ns]

5.2.5. Boolean Selection#

We have seen how we can select subsets of data by referring to the index or column names.

However, we often want to select based on conditions met by the data itself.

Some examples are:

Restrict analysis to all individuals older than 18.

Look at data that corresponds to particular time periods.

Analyze only data that corresponds to a recession.

Obtain data for a specific product or customer ID.

We will be able to do this by using a Series or list of boolean values to index into a Series or DataFrame.

Let’s look at some examples.

size_small = size.head() # Create smaller data so we can see what's happening

size_small

| industry | Autos | Banks | Meals | Softw | Smoke | Telcm | Mines |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 1926-07-31 | 47.55 | 14.50 | 10.82 | -99.99 | 59.72 | 350.36 | 27.74 |

| 1926-08-31 | 55.11 | 15.17 | 11.00 | -99.99 | 60.47 | 353.27 | 29.30 |

| 1926-09-30 | 57.11 | 16.97 | 10.94 | -99.99 | 64.03 | 360.96 | 29.45 |

| 1926-10-31 | 59.69 | 16.46 | 10.80 | -99.99 | 64.42 | 364.16 | 29.46 |

| 1926-11-30 | 54.81 | 14.52 | 10.33 | -99.99 | 65.08 | 363.74 | 28.51 |

# list of booleans selects rows

size_small.loc[[True, True, True, False, False]]

| industry | Autos | Banks | Meals | Softw | Smoke | Telcm | Mines |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 1926-07-31 | 47.55 | 14.50 | 10.82 | -99.99 | 59.72 | 350.36 | 27.74 |

| 1926-08-31 | 55.11 | 15.17 | 11.00 | -99.99 | 60.47 | 353.27 | 29.30 |

| 1926-09-30 | 57.11 | 16.97 | 10.94 | -99.99 | 64.03 | 360.96 | 29.45 |

# second argument selects columns, the ``:`` means "all".

# here we use it to select all columns

size_small.loc[[True, False, True, False, True], :]

| industry | Autos | Banks | Meals | Softw | Smoke | Telcm | Mines |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 1926-07-31 | 47.55 | 14.50 | 10.82 | -99.99 | 59.72 | 350.36 | 27.74 |

| 1926-09-30 | 57.11 | 16.97 | 10.94 | -99.99 | 64.03 | 360.96 | 29.45 |

| 1926-11-30 | 54.81 | 14.52 | 10.33 | -99.99 | 65.08 | 363.74 | 28.51 |

# can use booleans to select both rows and columns

size_small.loc[[True, True, True, False, False], [True, False, False, False, False, True, True]]

| industry | Autos | Telcm | Mines |

|---|---|---|---|

| Date | |||

| 1926-07-31 | 47.55 | 350.36 | 27.74 |

| 1926-08-31 | 55.11 | 353.27 | 29.30 |

| 1926-09-30 | 57.11 | 360.96 | 29.45 |

5.2.5.1. Creating Boolean DataFrames/Series#

We can use conditional statements to construct Series of booleans from our data.

size_small["Autos"] <55

Date

1926-07-31 True

1926-08-31 False

1926-09-30 False

1926-10-31 False

1926-11-30 True

Name: Autos, dtype: bool

Once we have our Series of bools, we can use it to extract subsets of rows from our DataFrame.

size_small.loc[size_small["Autos"] < 55]

| industry | Autos | Banks | Meals | Softw | Smoke | Telcm | Mines |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 1926-07-31 | 47.55 | 14.50 | 10.82 | -99.99 | 59.72 | 350.36 | 27.74 |

| 1926-11-30 | 54.81 | 14.52 | 10.33 | -99.99 | 65.08 | 363.74 | 28.51 |

size_small["Banks"] > size_small["Autos"]

Date

1926-07-31 False

1926-08-31 False

1926-09-30 False

1926-10-31 False

1926-11-30 False

dtype: bool

big_Autos = size_small["Autos"] > size_small["Banks"]

size_small.loc[big_Autos]

| industry | Autos | Banks | Meals | Softw | Smoke | Telcm | Mines |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 1926-07-31 | 47.55 | 14.50 | 10.82 | -99.99 | 59.72 | 350.36 | 27.74 |

| 1926-08-31 | 55.11 | 15.17 | 11.00 | -99.99 | 60.47 | 353.27 | 29.30 |

| 1926-09-30 | 57.11 | 16.97 | 10.94 | -99.99 | 64.03 | 360.96 | 29.45 |

| 1926-10-31 | 59.69 | 16.46 | 10.80 | -99.99 | 64.42 | 364.16 | 29.46 |

| 1926-11-30 | 54.81 | 14.52 | 10.33 | -99.99 | 65.08 | 363.74 | 28.51 |

5.2.5.1.1. Multiple Conditions#

In the boolean section of the basics lecture, we saw

that we can use the words and and or to combine multiple booleans into

a single bool.

Recall:

True and False -> FalseTrue and True -> TrueFalse and False -> FalseTrue or False -> TrueTrue or True -> TrueFalse or False -> False

We can do something similar in pandas, but instead of

bool1 and bool2 we write:

(bool_series1) & (bool_series2)

Likewise, instead of bool1 or bool2 we write:

(bool_series1) | (bool_series2)

small_BksAut = (size_small["Banks"] < 15) & (size_small["Autos"] < 56)

small_BksAut

Date

1926-07-31 True

1926-08-31 False

1926-09-30 False

1926-10-31 False

1926-11-30 True

dtype: bool

size_small[small_BksAut]

| industry | Autos | Banks | Meals | Softw | Smoke | Telcm | Mines |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 1926-07-31 | 47.55 | 14.50 | 10.82 | -99.99 | 59.72 | 350.36 | 27.74 |

| 1926-11-30 | 54.81 | 14.52 | 10.33 | -99.99 | 65.08 | 363.74 | 28.51 |

5.2.5.1.2. isin#

Sometimes, we will want to check whether a data point takes on one of a several fixed values.

We could do this by writing (df["x"] == val_1) | (df["x"] == val_2)

(like we did above), but there is a better way: the .isin method

size_small["Smoke"].isin([60.47, 64.42])

Date

1926-07-31 False

1926-08-31 True

1926-09-30 False

1926-10-31 True

1926-11-30 False

Name: Smoke, dtype: bool

# now select full rows where this Series is True

size_small.loc[size_small["Smoke"].isin([60.47, 64.42])]

| industry | Autos | Banks | Meals | Softw | Smoke | Telcm | Mines |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 1926-08-31 | 55.11 | 15.17 | 11.0 | -99.99 | 60.47 | 353.27 | 29.30 |

| 1926-10-31 | 59.69 | 16.46 | 10.8 | -99.99 | 64.42 | 364.16 | 29.46 |

5.2.5.1.3. .any and .all#

Recall from the boolean section of the basics lecture

that the Python functions any and all are aggregation functions that

take a collection of booleans and return a single boolean.

any returns True whenever at least one of the inputs are True while

all is True only when all the inputs are True.

Series and DataFrames with dtype bool have .any and .all

methods that apply this logic to pandas objects.

Let’s use these methods to count how many months all the states in our sample had low returns.

As we work through this example, consider the [“want operator”], a helpful concept from Nobel Laureate Tom Sargent for clearly stating the goal of our analysis and determining the steps necessary to reach the goal.

We always begin by writing Want: followed by what we want to

accomplish.

In this case, we would write:

Want: Count the number of months in which all industries in our sample had returns less than -5%

After identifying the want, we work backwards to identify the steps necessary to accomplish our goal.

So, starting from the result, we have:

Sum the number of

Truevalues in a Series indicating dates for which all industries had low returns.Build the Series used in the last step by using the

.allmethod on a DataFrame containing booleans indicating whether each industry had low returns at each date.Build the DataFrame used in the previous step using a

<comparison.

Now that we have a clear plan, let’s follow through and apply the want operator:

# Step 3: construct the DataFrame of bools

low = returns_all < -5

low.head()

| industry | Aero | Agric | Autos | Banks | Beer | BldMt | Books | Boxes | BusSv | Chems | ... | Smoke | Soda | Softw | Steel | Telcm | Toys | Trans | Txtls | Util | Whlsl |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||||

| 1926-07-31 | False | False | False | False | True | False | False | False | False | False | ... | False | True | True | False | False | False | False | False | False | True |

| 1926-08-31 | True | False | False | False | False | False | False | False | False | False | ... | False | True | True | False | False | False | False | False | False | False |

| 1926-09-30 | True | False | False | False | False | False | False | True | False | False | ... | False | True | True | False | False | False | False | False | False | True |

| 1926-10-31 | True | False | True | True | False | False | False | True | False | False | ... | False | True | True | False | False | False | False | False | False | True |

| 1926-11-30 | False | False | False | False | False | False | True | False | False | False | ... | False | True | True | False | False | False | False | False | False | False |

5 rows × 49 columns

# Step 2: use the .all method on axis=1 to get the dates where all states have a True

all_low = low.all(axis=1)

all_low.head()

Date

1926-07-31 False

1926-08-31 False

1926-09-30 False

1926-10-31 False

1926-11-30 False

dtype: bool

# Step 1: Call .sum to add up the number of True values in `all_low`

# (note that True == 1 and False == 0 in Python, so .sum will count Trues)

print(f'Out of {len(all_low)} months, {all_low.sum()} had low returns across all industries')

Out of 1137 months, 5 had low returns across all industries