4.12. Data APIs#

4.12.1. 🎯 Learning Objectives#

By the end of this notebook, you will be able to:

Access macroeconomic data — Using the FRED API

Explore alternative data — Google Trends and real-time stock prices

Download factor data — Ken French’s data library via pandas-datareader

Query institutional databases — WRDS for academic-quality financial data

4.12.2. 📋 Table of Contents#

4.12.3. 🛠️ Setup #

#@title 🛠️ Setup: Run this cell first (click to expand)

# Core libraries

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

%matplotlib inline

# Set consistent plot style

plt.style.use('seaborn-v0_8-whitegrid')

plt.rcParams['figure.figsize'] = [10, 6]

plt.rcParams['font.size'] = 12

# Suppress warnings for cleaner output

import warnings

warnings.filterwarnings('ignore')

print("✅ Core libraries loaded!")

✅ Core libraries loaded!

4.12.4. FRED API #

4.12.4.1. Federal Reserve Economic Data#

FRED is maintained by the Federal Reserve Bank of St. Louis and contains thousands of macroeconomic and financial time series.

Browse available data: https://fred.stlouisfed.org/categories

Example: 3-Month T-Bill yield: https://fred.stlouisfed.org/series/DTB3

Get your API key: https://research.stlouisfed.org/docs/api/api_key.html

# Install fredapi - a Python wrapper for the FRED API

# This library lets you download economic data directly into pandas DataFrames

!pip install fredapi

Collecting fredapi

Downloading fredapi-0.5.2-py3-none-any.whl.metadata (5.0 kB)

Requirement already satisfied: pandas in /usr/local/lib/python3.12/dist-packages (from fredapi) (2.2.2)

Requirement already satisfied: numpy>=1.26.0 in /usr/local/lib/python3.12/dist-packages (from pandas->fredapi) (2.0.2)

Requirement already satisfied: python-dateutil>=2.8.2 in /usr/local/lib/python3.12/dist-packages (from pandas->fredapi) (2.9.0.post0)

Requirement already satisfied: pytz>=2020.1 in /usr/local/lib/python3.12/dist-packages (from pandas->fredapi) (2025.2)

Requirement already satisfied: tzdata>=2022.7 in /usr/local/lib/python3.12/dist-packages (from pandas->fredapi) (2025.3)

Requirement already satisfied: six>=1.5 in /usr/local/lib/python3.12/dist-packages (from python-dateutil>=2.8.2->pandas->fredapi) (1.17.0)

Downloading fredapi-0.5.2-py3-none-any.whl (11 kB)

Installing collected packages: fredapi

Successfully installed fredapi-0.5.2

from fredapi import Fred

# Initialize with API key

fred = Fred(api_key='f9207136b3333d7cf92c07273f6f5530')

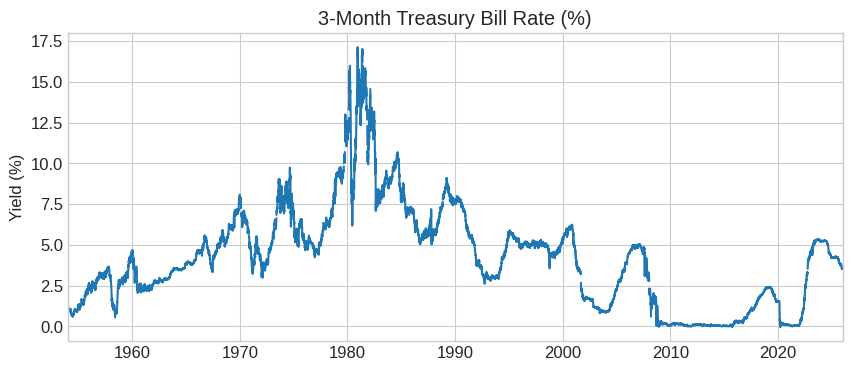

# Download 3-Month T-Bill rate

tbill_3m = fred.get_series('DTB3')

tbill_3m.plot(title='3-Month Treasury Bill Rate (%)', figsize=(10, 4))

plt.ylabel('Yield (%)')

plt.show()

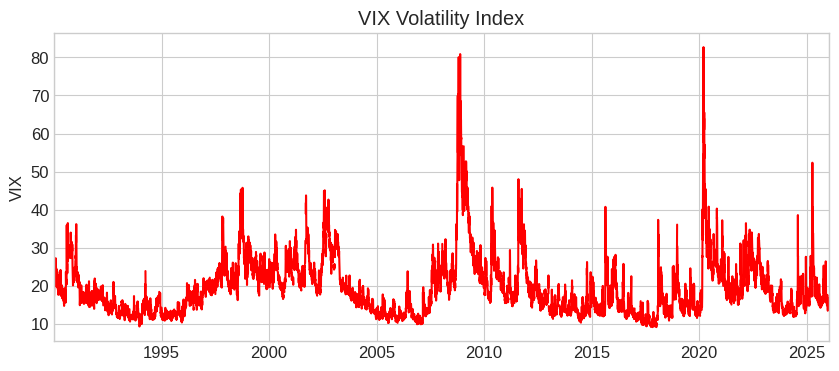

# Download VIX - the "fear index"

vix = fred.get_series('VIXCLS')

vix.plot(title='VIX Volatility Index', figsize=(10, 4), color='red')

plt.ylabel('VIX')

plt.show()

💡 Key Insight:

FRED is your go-to source for macroeconomic data: interest rates, GDP, unemployment, inflation, and more. All free with an API key!

4.12.5. Google Trends #

4.12.5.1. Alternative Data: Search Interest#

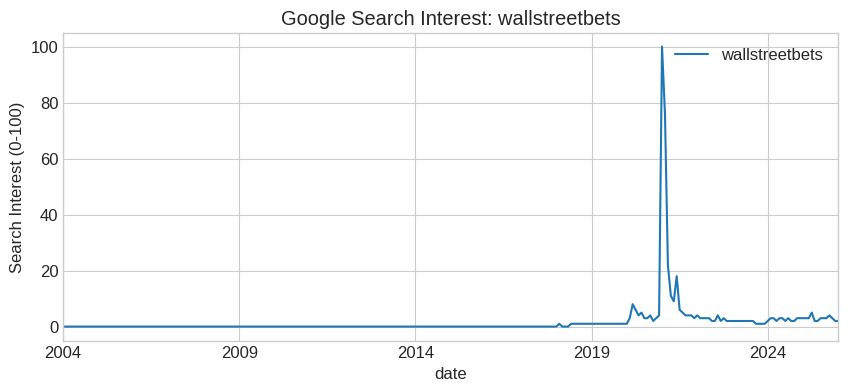

Google Trends provides data on search interest over time. This is an example of alternative data — non-traditional data sources that can provide unique insights.

Here I am going to get data from https://serpapi.com/

You can sign up for a free account to get an API_KEY

It allows you to tap all sort of information form Google. Here we will use to get google_trends

Google_trends is often use as a proxy for attention of retail investors

!pip install google-search-results

from serpapi import GoogleSearch

import pandas as pd

import matplotlib.pyplot as plt

# ⚠️ Uncomment the lines below after adding your API Key

#API_KEY='a8667ee3d37e1dd2990c4084515c73d0a53fa6a2bad51fd03afbdcac7a8b9f9d'

# this gives parameters to the API

params = {

"api_key": API_KEY,

"engine": "google_trends",

"q": "GME",

"date": "all"

}

# This calls the API

search = GoogleSearch(params)

results = search.get_dict()

# now we need to put this in format that is good for plotting

# Extract timeline data from the dictionary and put it dataframe format

timeline = results.get('interest_over_time', {}).get('timeline_data', [])

records = []

for point in timeline:

row = {'date': point['date']}

row.update({v['query']: v['extracted_value'] for v in point['values']})

records.append(row)

df = pd.DataFrame(records)

# Plot

df['date'] = pd.to_datetime(df['date'])

df.set_index('date').plot(title='Google Search Interest: wallstreetbets', figsize=(10, 4))

plt.ylabel('Search Interest (0-100)')

plt.show()

📌 Remember:

Google Trends can signal retail investor interest. The GME spike in early 2021 coincided with the famous “meme stock” rally driven by Reddit.

4.12.6. WallStreet: Real-Time Stock Data #

4.12.6.1. Real-Time Prices and Historical Data#

The wallstreet library provides real-time stock quotes and historical data. It also supports options data (calls and puts).

Documentation: mcdallas/wallstreet

# Install wallstreet - real-time stock and options data

# Provides current prices, historical data, and options chains without an API key

!pip install yfinance

Requirement already satisfied: yfinance in /usr/local/lib/python3.12/dist-packages (0.2.66)

Requirement already satisfied: pandas>=1.3.0 in /usr/local/lib/python3.12/dist-packages (from yfinance) (2.2.2)

Requirement already satisfied: numpy>=1.16.5 in /usr/local/lib/python3.12/dist-packages (from yfinance) (2.0.2)

Requirement already satisfied: requests>=2.31 in /usr/local/lib/python3.12/dist-packages (from yfinance) (2.32.4)

Requirement already satisfied: multitasking>=0.0.7 in /usr/local/lib/python3.12/dist-packages (from yfinance) (0.0.12)

Requirement already satisfied: platformdirs>=2.0.0 in /usr/local/lib/python3.12/dist-packages (from yfinance) (4.5.1)

Requirement already satisfied: pytz>=2022.5 in /usr/local/lib/python3.12/dist-packages (from yfinance) (2025.2)

Requirement already satisfied: frozendict>=2.3.4 in /usr/local/lib/python3.12/dist-packages (from yfinance) (2.4.7)

Requirement already satisfied: peewee>=3.16.2 in /usr/local/lib/python3.12/dist-packages (from yfinance) (3.19.0)

Requirement already satisfied: beautifulsoup4>=4.11.1 in /usr/local/lib/python3.12/dist-packages (from yfinance) (4.13.5)

Requirement already satisfied: curl_cffi>=0.7 in /usr/local/lib/python3.12/dist-packages (from yfinance) (0.14.0)

Requirement already satisfied: protobuf>=3.19.0 in /usr/local/lib/python3.12/dist-packages (from yfinance) (5.29.5)

Requirement already satisfied: websockets>=13.0 in /usr/local/lib/python3.12/dist-packages (from yfinance) (15.0.1)

Requirement already satisfied: soupsieve>1.2 in /usr/local/lib/python3.12/dist-packages (from beautifulsoup4>=4.11.1->yfinance) (2.8.1)

Requirement already satisfied: typing-extensions>=4.0.0 in /usr/local/lib/python3.12/dist-packages (from beautifulsoup4>=4.11.1->yfinance) (4.15.0)

Requirement already satisfied: cffi>=1.12.0 in /usr/local/lib/python3.12/dist-packages (from curl_cffi>=0.7->yfinance) (2.0.0)

Requirement already satisfied: certifi>=2024.2.2 in /usr/local/lib/python3.12/dist-packages (from curl_cffi>=0.7->yfinance) (2026.1.4)

Requirement already satisfied: python-dateutil>=2.8.2 in /usr/local/lib/python3.12/dist-packages (from pandas>=1.3.0->yfinance) (2.9.0.post0)

Requirement already satisfied: tzdata>=2022.7 in /usr/local/lib/python3.12/dist-packages (from pandas>=1.3.0->yfinance) (2025.3)

Requirement already satisfied: charset_normalizer<4,>=2 in /usr/local/lib/python3.12/dist-packages (from requests>=2.31->yfinance) (3.4.4)

Requirement already satisfied: idna<4,>=2.5 in /usr/local/lib/python3.12/dist-packages (from requests>=2.31->yfinance) (3.11)

Requirement already satisfied: urllib3<3,>=1.21.1 in /usr/local/lib/python3.12/dist-packages (from requests>=2.31->yfinance) (2.5.0)

Requirement already satisfied: pycparser in /usr/local/lib/python3.12/dist-packages (from cffi>=1.12.0->curl_cffi>=0.7->yfinance) (2.23)

Requirement already satisfied: six>=1.5 in /usr/local/lib/python3.12/dist-packages (from python-dateutil>=2.8.2->pandas>=1.3.0->yfinance) (1.17.0)

import yfinance as yf

# Single stock - current price

gme = yf.Ticker('GME')

print(f"GME current price: ${gme.info['currentPrice']:.2f}")

# Historical data (returns a DataFrame!)

df = gme.history(period='max') # or '5y', 'max', etc.

print(df.head())

# Quick plot

df['Close'].plot(title='GME Price History', figsize=(10, 4))

GME current price: $21.10

Open High Low Close Volume \

Date

2002-02-13 00:00:00-05:00 1.620128 1.693350 1.603296 1.691667 76216000

2002-02-14 00:00:00-05:00 1.712707 1.716073 1.670626 1.683250 11021600

2002-02-15 00:00:00-05:00 1.683250 1.687458 1.658001 1.674834 8389600

2002-02-19 00:00:00-05:00 1.666418 1.666418 1.578047 1.607504 7410400

2002-02-20 00:00:00-05:00 1.615920 1.662210 1.603296 1.662210 6892800

Dividends Stock Splits

Date

2002-02-13 00:00:00-05:00 0.0 0.0

2002-02-14 00:00:00-05:00 0.0 0.0

2002-02-15 00:00:00-05:00 0.0 0.0

2002-02-19 00:00:00-05:00 0.0 0.0

2002-02-20 00:00:00-05:00 0.0 0.0

<Axes: title={'center': 'GME Price History'}, xlabel='Date'>

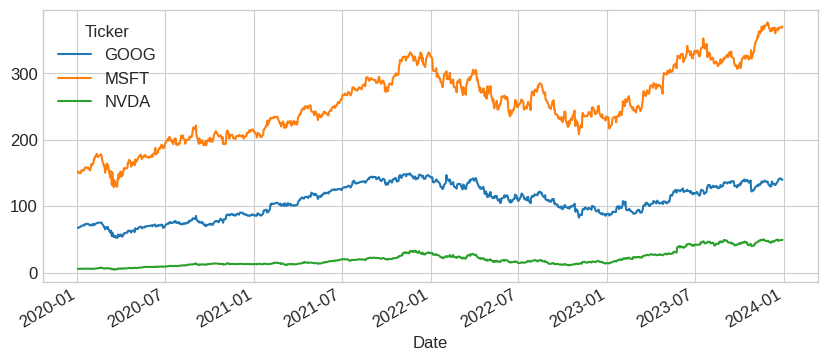

df = yf.download(['NVDA', 'MSFT', 'GOOG'], start='2020-01-01', end='2024-01-01')

df['Close'].plot(figsize=(10, 4))

[*********************100%***********************] 3 of 3 completed

<Axes: xlabel='Date'>

4.12.7. Pandas DataReader: Ken French Library #

4.12.7.1. Academic Factor Data#

Pandas DataReader connects to many data sources. We’re most interested in Ken French’s data library, which provides returns on factor portfolios used in academic finance.

Documentation: https://pandas-datareader.readthedocs.io/en/latest/remote_data.html

# Install pandas-datareader - connects to various financial data sources

# Key feature: access to Ken French's factor data library (297 datasets!)

!pip install pandas_datareader

Requirement already satisfied: pandas_datareader in /usr/local/lib/python3.12/dist-packages (0.10.0)

Requirement already satisfied: lxml in /usr/local/lib/python3.12/dist-packages (from pandas_datareader) (6.0.2)

Requirement already satisfied: pandas>=0.23 in /usr/local/lib/python3.12/dist-packages (from pandas_datareader) (2.2.2)

Requirement already satisfied: requests>=2.19.0 in /usr/local/lib/python3.12/dist-packages (from pandas_datareader) (2.32.4)

Requirement already satisfied: numpy>=1.26.0 in /usr/local/lib/python3.12/dist-packages (from pandas>=0.23->pandas_datareader) (2.0.2)

Requirement already satisfied: python-dateutil>=2.8.2 in /usr/local/lib/python3.12/dist-packages (from pandas>=0.23->pandas_datareader) (2.9.0.post0)

Requirement already satisfied: pytz>=2020.1 in /usr/local/lib/python3.12/dist-packages (from pandas>=0.23->pandas_datareader) (2025.2)

Requirement already satisfied: tzdata>=2022.7 in /usr/local/lib/python3.12/dist-packages (from pandas>=0.23->pandas_datareader) (2025.3)

Requirement already satisfied: charset_normalizer<4,>=2 in /usr/local/lib/python3.12/dist-packages (from requests>=2.19.0->pandas_datareader) (3.4.4)

Requirement already satisfied: idna<4,>=2.5 in /usr/local/lib/python3.12/dist-packages (from requests>=2.19.0->pandas_datareader) (3.11)

Requirement already satisfied: urllib3<3,>=1.21.1 in /usr/local/lib/python3.12/dist-packages (from requests>=2.19.0->pandas_datareader) (2.5.0)

Requirement already satisfied: certifi>=2017.4.17 in /usr/local/lib/python3.12/dist-packages (from requests>=2.19.0->pandas_datareader) (2026.1.4)

Requirement already satisfied: six>=1.5 in /usr/local/lib/python3.12/dist-packages (from python-dateutil>=2.8.2->pandas>=0.23->pandas_datareader) (1.17.0)

from pandas_datareader.famafrench import get_available_datasets

# How many datasets are available?

datasets = get_available_datasets()

print(f"Ken French Library has {len(datasets)} datasets!")

Ken French Library has 297 datasets!

from datetime import datetime

import pandas_datareader.data as web

# Download the 49 Industry Portfolios

start = datetime(1926, 1, 1)

ds = web.DataReader('49_Industry_Portfolios', 'famafrench', start=start)

# See what's included

print(ds['DESCR'])

49 Industry Portfolios

----------------------

This file was created using the 202511 CRSP database. It contains value- and equal-weighted returns for 49 industry portfolios. The portfolios are constructed at the end of June. The annual returns are from January to December. Missing data are indicated by -99.99 or -999. Copyright 2025 Eugene F. Fama and Kenneth R. French

0 : Average Value Weighted Returns -- Monthly (1193 rows x 49 cols)

1 : Average Equal Weighted Returns -- Monthly (1193 rows x 49 cols)

2 : Average Value Weighted Returns -- Annual (98 rows x 49 cols)

3 : Average Equal Weighted Returns -- Annual (98 rows x 49 cols)

4 : Number of Firms in Portfolios (1193 rows x 49 cols)

5 : Average Firm Size (1193 rows x 49 cols)

6 : Sum of BE / Sum of ME (100 rows x 49 cols)

7 : Value-Weighted Average of BE/ME (100 rows x 49 cols)

The dataset contains 7 different tables:

Index |

Contents |

|---|---|

0 |

Value-weighted monthly returns |

1 |

Equal-weighted monthly returns |

2 |

Value-weighted annual returns |

… |

… |

6 |

Book-to-market ratios |

# Get value-weighted monthly returns (index 0)

industry_returns = ds[0]

industry_returns.tail()

| Agric | Food | Soda | Beer | Smoke | Toys | Fun | Books | Hshld | Clths | ... | Boxes | Trans | Whlsl | Rtail | Meals | Banks | Insur | RlEst | Fin | Other | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||||

| 2025-07 | -1.94 | -0.38 | -4.12 | 3.38 | -5.84 | 2.04 | -8.73 | -3.33 | -3.10 | 2.51 | ... | -0.42 | -2.06 | 0.14 | 3.11 | -2.51 | 0.82 | -9.74 | 10.67 | 4.49 | -2.32 |

| 2025-08 | 2.81 | 0.13 | 3.43 | 3.49 | 3.87 | 6.39 | 5.00 | 5.69 | 3.27 | 4.25 | ... | 1.99 | 4.21 | 1.54 | 0.85 | 0.88 | 5.11 | 7.49 | 5.79 | -0.20 | 4.46 |

| 2025-09 | -9.46 | -1.77 | -1.54 | -7.12 | -2.09 | -3.06 | -1.69 | 0.91 | -3.54 | -5.42 | ... | -3.89 | 0.49 | 0.80 | -1.06 | -4.61 | 0.13 | 1.63 | -3.50 | 2.96 | -0.75 |

| 2025-10 | -8.64 | -5.43 | 3.16 | 3.37 | -11.53 | 0.73 | -6.36 | -8.03 | -3.04 | -6.04 | ... | -7.86 | -0.24 | 0.02 | 2.85 | -3.60 | -0.10 | -6.36 | -1.88 | -2.97 | -4.21 |

| 2025-11 | 8.12 | 3.14 | 6.20 | 2.36 | 7.82 | 9.20 | -1.53 | 2.25 | 1.14 | 3.88 | ... | 4.45 | 0.55 | 1.77 | -0.42 | 6.60 | 1.35 | 3.30 | 7.15 | 0.29 | 6.18 |

5 rows × 49 columns

# Get book-to-market ratios (index 6)

book_to_market = ds[6]

book_to_market.tail()

| Agric | Food | Soda | Beer | Smoke | Toys | Fun | Books | Hshld | Clths | ... | Boxes | Trans | Whlsl | Rtail | Meals | Banks | Insur | RlEst | Fin | Other | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||||

| 2021 | 0.85 | 0.41 | 0.09 | 0.17 | -0.05 | 0.10 | 0.10 | 0.55 | 0.12 | 0.13 | ... | 0.30 | 0.17 | 0.24 | 0.12 | 0.01 | 0.64 | 0.65 | 0.32 | 0.45 | 0.66 |

| 2022 | 0.71 | 0.39 | 0.10 | 0.18 | -0.05 | 0.20 | 0.11 | 0.50 | 0.11 | 0.13 | ... | 0.32 | 0.17 | 0.21 | 0.11 | 0.02 | 0.53 | 0.51 | 0.29 | 0.36 | 0.63 |

| 2023 | 0.62 | 0.40 | 0.10 | 0.16 | -0.05 | 0.40 | 0.19 | 0.67 | 0.17 | 0.17 | ... | 0.43 | 0.23 | 0.24 | 0.15 | 0.01 | 0.64 | 0.35 | 0.34 | 0.40 | 0.59 |

| 2024 | 0.75 | 0.44 | 0.11 | 0.21 | -0.07 | 0.31 | 0.15 | 0.51 | 0.16 | 0.18 | ... | 0.41 | 0.19 | 0.21 | 0.13 | 0.02 | 0.71 | 0.39 | 0.37 | 0.36 | 0.58 |

| 2025 | 0.60 | 0.48 | 0.10 | 0.24 | -0.05 | 0.31 | 0.10 | 0.44 | 0.15 | 0.22 | ... | 0.35 | 0.20 | 0.19 | 0.11 | 0.01 | 0.57 | 0.38 | 0.32 | 0.31 | 0.58 |

5 rows × 49 columns

4.12.7.2. Browsing All Available Datasets#

# View first 20 available datasets

print("First 20 Ken French datasets:")

for i, name in enumerate(datasets[:20]):

print(f" {i+1}. {name}")

First 20 Ken French datasets:

1. F-F_Research_Data_Factors

2. F-F_Research_Data_Factors_weekly

3. F-F_Research_Data_Factors_daily

4. F-F_Research_Data_5_Factors_2x3

5. F-F_Research_Data_5_Factors_2x3_daily

6. Portfolios_Formed_on_ME

7. Portfolios_Formed_on_ME_Wout_Div

8. Portfolios_Formed_on_ME_Daily

9. Portfolios_Formed_on_BE-ME

10. Portfolios_Formed_on_BE-ME_Wout_Div

11. Portfolios_Formed_on_BE-ME_Daily

12. Portfolios_Formed_on_OP

13. Portfolios_Formed_on_OP_Wout_Div

14. Portfolios_Formed_on_OP_Daily

15. Portfolios_Formed_on_INV

16. Portfolios_Formed_on_INV_Wout_Div

17. Portfolios_Formed_on_INV_Daily

18. 6_Portfolios_2x3

19. 6_Portfolios_2x3_Wout_Div

20. 6_Portfolios_2x3_weekly

💡 Key Insight:

Ken French’s library is the gold standard for factor research. It includes Fama-French factors, momentum, industry portfolios, and more.

4.12.8. WRDS: Academic Financial Data #

4.12.8.1. The Gold Standard for Research#

WRDS (Wharton Research Data Services) is the premier source for academic financial data. It includes:

CRSP: Stock prices, returns, and market data

Compustat: Balance sheet and income statement data

IBES: Analyst forecasts

And much more…

Register for an account: https://wrds-www.wharton.upenn.edu/register/

# Install WRDS library - official Python interface for WRDS database

# Requires a WRDS account (free for academic users)

!pip install wrds

Collecting wrds

Downloading wrds-3.4.0-py3-none-any.whl.metadata (5.7 kB)

Collecting packaging<=24.2 (from wrds)

Downloading packaging-24.2-py3-none-any.whl.metadata (3.2 kB)

Requirement already satisfied: pandas<2.3,>=2.2 in /usr/local/lib/python3.12/dist-packages (from wrds) (2.2.2)

Collecting psycopg2-binary<2.10,>=2.9 (from wrds)

Downloading psycopg2_binary-2.9.11-cp312-cp312-manylinux2014_x86_64.manylinux_2_17_x86_64.whl.metadata (4.9 kB)

Requirement already satisfied: sqlalchemy<2.1,>=2 in /usr/local/lib/python3.12/dist-packages (from wrds) (2.0.45)

Requirement already satisfied: numpy>=1.26.0 in /usr/local/lib/python3.12/dist-packages (from pandas<2.3,>=2.2->wrds) (2.0.2)

Requirement already satisfied: python-dateutil>=2.8.2 in /usr/local/lib/python3.12/dist-packages (from pandas<2.3,>=2.2->wrds) (2.9.0.post0)

Requirement already satisfied: pytz>=2020.1 in /usr/local/lib/python3.12/dist-packages (from pandas<2.3,>=2.2->wrds) (2025.2)

Requirement already satisfied: tzdata>=2022.7 in /usr/local/lib/python3.12/dist-packages (from pandas<2.3,>=2.2->wrds) (2025.3)

Requirement already satisfied: greenlet>=1 in /usr/local/lib/python3.12/dist-packages (from sqlalchemy<2.1,>=2->wrds) (3.3.0)

Requirement already satisfied: typing-extensions>=4.6.0 in /usr/local/lib/python3.12/dist-packages (from sqlalchemy<2.1,>=2->wrds) (4.15.0)

Requirement already satisfied: six>=1.5 in /usr/local/lib/python3.12/dist-packages (from python-dateutil>=2.8.2->pandas<2.3,>=2.2->wrds) (1.17.0)

Downloading wrds-3.4.0-py3-none-any.whl (14 kB)

Downloading packaging-24.2-py3-none-any.whl (65 kB)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━ 65.5/65.5 kB 5.4 MB/s eta 0:00:00

?25hDownloading psycopg2_binary-2.9.11-cp312-cp312-manylinux2014_x86_64.manylinux_2_17_x86_64.whl (4.2 MB)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━ 4.2/4.2 MB 57.4 MB/s eta 0:00:00

?25hInstalling collected packages: psycopg2-binary, packaging, wrds

Attempting uninstall: packaging

Found existing installation: packaging 25.0

Uninstalling packaging-25.0:

Successfully uninstalled packaging-25.0

Successfully installed packaging-24.2 psycopg2-binary-2.9.11 wrds-3.4.0

import wrds

import psycopg2

# Connect to WRDS (will prompt for username/password)

conn = wrds.Connection()

Enter your WRDS username [root]:am16634

Enter your password:··········

WRDS recommends setting up a .pgpass file.

Create .pgpass file now [y/n]?: y

Created .pgpass file successfully.

You can create this file yourself at any time with the create_pgpass_file() function.

Loading library list...

Done

4.12.8.2. Downloading Stock Returns#

WRDS uses SQL queries to access data. Here’s a function to download daily returns for a given stock:

def get_returns(tickers, conn, startdate, enddate):

"""Download daily returns for a list of tickers from WRDS CRSP."""

ticker = tickers[0]

df = conn.raw_sql("""

select a.permno, b.ticker, a.date, a.ret

from crsp.dsf as a

left join crsp.msenames as b

on a.permno=b.permno

and b.namedt<=a.date

and a.date<=b.nameendt

where a.date between '""" + startdate + """' and '""" + enddate + """'

and b.ticker='""" + ticker + "'")

df.set_index(['date', 'permno'], inplace=True)

df = df['ret'].unstack()

return df

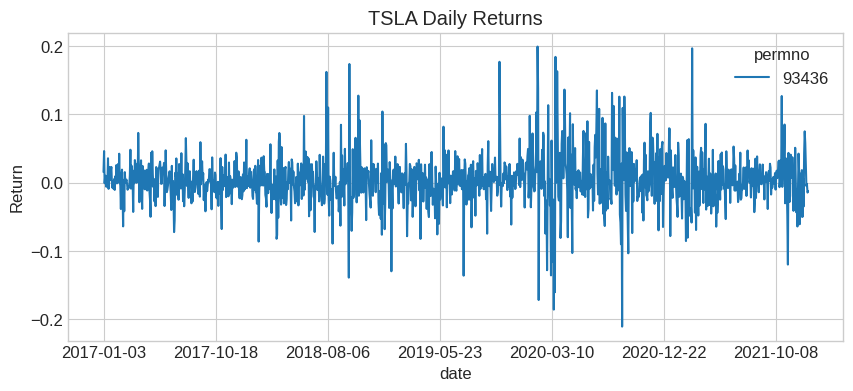

# Download Tesla returns

df_tsla = get_returns(['TSLA'], conn, '1/1/2017', '1/1/2022')

df_tsla.plot(title='TSLA Daily Returns', figsize=(10, 4))

plt.ylabel('Return')

plt.show()

4.12.8.3. Getting Price and Shares Outstanding#

def get_data(tickers, conn, startdate, enddate):

"""Download price and shares outstanding from WRDS CRSP."""

ticker = tickers[0]

df = conn.raw_sql("""

select a.permno, b.ticker, a.date, a.prc, a.shrout

from crsp.dsf as a

left join crsp.msenames as b

on a.permno=b.permno

and b.namedt<=a.date

and a.date<=b.nameendt

where a.date between '""" + startdate + """' and '""" + enddate + """'

and b.ticker='""" + ticker + "'")

df.set_index(['date', 'permno'], inplace=True)

return df

# Download Tesla price data

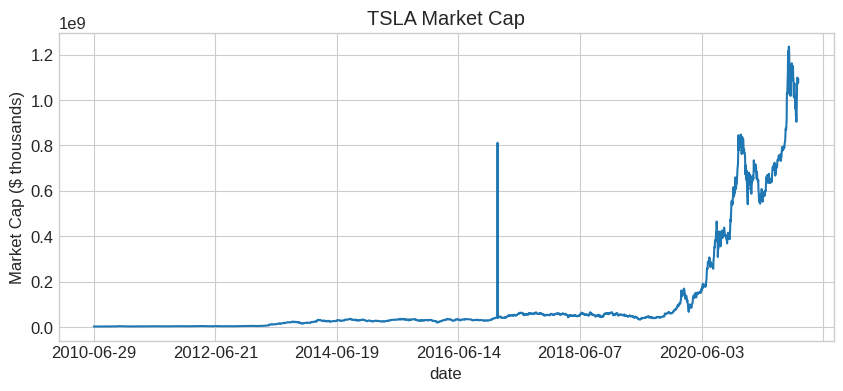

df = get_data(['TSLA'], conn, '1/1/2005', '1/1/2022')

# Compute market cap (price uses absolute value because negative = bid-ask midpoint)

df['mcap'] = df['prc'].abs() * df['shrout']

# Clean up index and plot

df = df.reset_index().set_index('date')

df['mcap'].plot(title='TSLA Market Cap', figsize=(10, 4))

plt.ylabel('Market Cap ($ thousands)')

plt.show()

📌 Remember:

WRDS variables in CRSP:

ret: daily return (with dividends)

prc: price (negative = bid-ask midpoint). When there was not trade at closing–zero probability for Tesla or any large cap

shrout: shares outstanding (thousands)

vol: trading volume (shares)

4.12.9. 📝 Exercises #

4.12.9.1. Exercise 1: Warm-up — Explore FRED#

🔧 Exercise:

Use the FRED API to:

Download the 10-Year Treasury yield (

GS10)Download the unemployment rate (

UNRATE)Plot both series on the same figure (use two y-axes)

What pattern do you observe during recessions?

# Your code here

💡 Click to see solution

# Download data

gs10 = fred.get_series('GS10')

unrate = fred.get_series('UNRATE')

# Plot with two y-axes

fig, ax1 = plt.subplots(figsize=(12, 5))

ax1.plot(gs10.index, gs10, color='blue', label='10-Year Treasury')

ax1.set_ylabel('10Y Yield (%)', color='blue')

ax2 = ax1.twinx()

ax2.plot(unrate.index, unrate, color='red', label='Unemployment')

ax2.set_ylabel('Unemployment Rate (%)', color='red')

plt.title('Interest Rates vs. Unemployment')

plt.show()

# During recessions: unemployment spikes, rates often fall

4.12.9.2. Exercise 2: Extension — Ken French Factor Data#

🤔 Think and Code:

Download the Fama-French 3-Factor data:

Use

web.DataReader('F-F_Research_Data_Factors', 'famafrench')Extract the monthly factors (index 0)

Plot cumulative returns of MKT-RF, SMB, and HML since 1926

Which factor had the highest cumulative return? Which had the most volatility?

# Your code here

💡 Click to see solution

# Download Fama-French factors

ff = web.DataReader('F-F_Research_Data_Factors', 'famafrench', start=datetime(1926,1,1))

factors = ff[0] / 100 # Convert from percentage to decimal

# Compute cumulative returns

cum_returns = (1 + factors[['Mkt-RF', 'SMB', 'HML']]).cumprod()

# Plot

cum_returns.plot(figsize=(12, 6), title='Cumulative Factor Returns Since 1926')

plt.ylabel('Cumulative Return ($1 initial)')

plt.yscale('log')

plt.legend(['Market-RF', 'Small-Big', 'High-Low B/M'])

plt.show()

# Summary statistics

print("Annualized Statistics:")

print(f"MKT-RF: mean={factors['Mkt-RF'].mean()*12:.2%}, std={factors['Mkt-RF'].std()*np.sqrt(12):.2%}")

print(f"SMB: mean={factors['SMB'].mean()*12:.2%}, std={factors['SMB'].std()*np.sqrt(12):.2%}")

print(f"HML: mean={factors['HML'].mean()*12:.2%}, std={factors['HML'].std()*np.sqrt(12):.2%}")

4.12.9.3. Exercise 3: Open-ended — Industry Analysis#

🤔 Think and Code:

Using the 49 Industry Portfolios:

Compute the annualized mean and volatility for each industry

Create a scatter plot of mean vs. volatility (each point = one industry)

Which industries have the best risk-adjusted returns (highest Sharpe)?

Which industries are the most volatile?

# Your code here

💡 Click to see solution

# Get industry returns (already loaded as ds[0])

ind_ret = ds[0] / 100 # Convert to decimal

# Compute annualized statistics

ind_mean = ind_ret.mean() * 12

ind_std = ind_ret.std() * np.sqrt(12)

ind_sharpe = ind_mean / ind_std

# Scatter plot

fig, ax = plt.subplots(figsize=(10, 8))

ax.scatter(ind_std, ind_mean, alpha=0.7)

# Label each point

for i, ind in enumerate(ind_ret.columns):

ax.annotate(ind, (ind_std[ind], ind_mean[ind]), fontsize=8)

ax.set_xlabel('Annualized Volatility')

ax.set_ylabel('Annualized Mean Return')

ax.set_title('Industry Risk-Return Tradeoff')

plt.show()

# Top 5 by Sharpe

print("Top 5 industries by Sharpe Ratio:")

print(ind_sharpe.nlargest(5))

4.12.10. 🧠 Key Takeaways #

FRED — Free macroeconomic data (rates, GDP, unemployment) via

fredapiGoogle Trends — Alternative data on search interest via

pytrendsWallStreet — Real-time stock/options quotes via

wallstreetKen French Library — 297 factor/portfolio datasets via

pandas-datareaderWRDS — Academic-quality financial data (requires registration)