5.6. Expected Returns Timing#

5.6.1. 🎯 Learning Objectives#

By the end of this notebook, you will be able to:

Understand return predictability — Why dividend yields might forecast future stock returns

Run and interpret forecasting regressions — Test if a signal predicts returns using proper inference

Evaluate predictability out-of-sample — Use R² comparisons and trading strategies

Construct timing strategies — Convert signals into portfolio weights

Assess timing performance — Use alpha, Sharpe ratios, and proper benchmarks

5.6.2. 📋 Table of Contents#

5.6.3. 🛠️ Setup #

#@title 🛠️ Setup: Run this cell first (click to expand)

# Core libraries

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

%matplotlib inline

# statsmodels: Statistical modeling for Python

# Provides OLS regression with robust standard errors (HAC)

!pip install statsmodels

import statsmodels.api as sm

# pandas-datareader: Fetches financial data from online sources

from pandas_datareader import data as DataReader

# Set consistent plot style

plt.style.use('seaborn-v0_8-whitegrid')

plt.rcParams['figure.figsize'] = [10, 6]

plt.rcParams['font.size'] = 12

# Suppress warnings for cleaner output

import warnings

warnings.filterwarnings('ignore')

print("✅ Libraries loaded successfully!")

Requirement already satisfied: statsmodels in /usr/local/lib/python3.12/dist-packages (0.14.6)

Requirement already satisfied: numpy<3,>=1.22.3 in /usr/local/lib/python3.12/dist-packages (from statsmodels) (2.0.2)

Requirement already satisfied: scipy!=1.9.2,>=1.8 in /usr/local/lib/python3.12/dist-packages (from statsmodels) (1.16.3)

Requirement already satisfied: pandas!=2.1.0,>=1.4 in /usr/local/lib/python3.12/dist-packages (from statsmodels) (2.2.2)

Requirement already satisfied: patsy>=0.5.6 in /usr/local/lib/python3.12/dist-packages (from statsmodels) (1.0.2)

Requirement already satisfied: packaging>=21.3 in /usr/local/lib/python3.12/dist-packages (from statsmodels) (25.0)

Requirement already satisfied: python-dateutil>=2.8.2 in /usr/local/lib/python3.12/dist-packages (from pandas!=2.1.0,>=1.4->statsmodels) (2.9.0.post0)

Requirement already satisfied: pytz>=2020.1 in /usr/local/lib/python3.12/dist-packages (from pandas!=2.1.0,>=1.4->statsmodels) (2025.2)

Requirement already satisfied: tzdata>=2022.7 in /usr/local/lib/python3.12/dist-packages (from pandas!=2.1.0,>=1.4->statsmodels) (2025.3)

Requirement already satisfied: six>=1.5 in /usr/local/lib/python3.12/dist-packages (from python-dateutil>=2.8.2->pandas!=2.1.0,>=1.4->statsmodels) (1.17.0)

✅ Libraries loaded successfully!

#@title Helper Function: Get Factor Data

def get_factors(factors='CAPM', freq='daily'):

"""

Fetch Fama-French factor data from Ken French's website.

Parameters:

-----------

factors : str

'CAPM' (RF, Mkt-RF), 'FF3', 'FF5', or 'FF6'

freq : str

'daily' or 'monthly'

"""

freq_label = '' if freq == 'monthly' else '_' + freq

if factors == 'CAPM':

ff = DataReader.DataReader(f"F-F_Research_Data_Factors{freq_label}",

"famafrench", start="1921-01-01")

df_factor = ff[0][['RF', 'Mkt-RF']]

else:

ff = DataReader.DataReader(f"F-F_Research_Data_Factors{freq_label}",

"famafrench", start="1921-01-01")

df_factor = ff[0][['RF', 'Mkt-RF', 'SMB', 'HML']]

if freq == 'monthly':

df_factor.index = pd.to_datetime(df_factor.index.to_timestamp() + pd.offsets.MonthEnd(0))

else:

df_factor.index = pd.to_datetime(df_factor.index)

return df_factor / 100

5.6.4. The Predictability Puzzle #

5.6.4.1. The Classic Finding#

One of the most famous findings in finance:

High dividend yield periods are followed by above-average returns

This finding earned Robert Shiller a Nobel Prize! 🏆

5.6.4.2. Why is This Surprising?#

When prices are low (relative to dividends), you might expect:

❌ Future dividends will fall → “Bad news is priced in”

But what actually happens:

✅ Future prices go up → Expected returns were high!

This suggests expected returns vary over time.

Intution is super general but you can see it in the simple Gordon growth formula

Implies

So if dividend yield is low is either becasue

Expected returns are low or expected growth is high

💡 Key Insight:

If expected returns are time-varying and predictable, you can build timing strategies that invest more when expected returns are high.

5.6.5. Dividend Yield as a Signal #

5.6.5.1. Loading Market Data#

# Load CRSP market data with dividend yield

url = 'https://raw.githubusercontent.com/amoreira2/UG54/refs/heads/main/assets/data/Markettiming_data1.csv'

crsp = pd.read_csv(url, parse_dates=['date'], index_col='date')

print(f"Data range: {crsp.index.min().date()} to {crsp.index.max().date()}")

crsp.head()

Data range: 1925-12-31 to 2024-12-31

| vwretd | vwretx | dp | |

|---|---|---|---|

| date | |||

| 1925-12-31 | NaN | NaN | NaN |

| 1926-01-30 | 0.000561 | -0.001395 | 0.001959 |

| 1926-02-27 | -0.033046 | -0.036587 | 0.003675 |

| 1926-03-31 | -0.064002 | -0.070021 | 0.006472 |

| 1926-04-30 | 0.037029 | 0.034043 | 0.002888 |

The data contains:

vwretd: Value-weighted market return (with dividends)vwretx: Value-weighted market return (without dividends)dp: Dividend yield (dividend/price ratio)

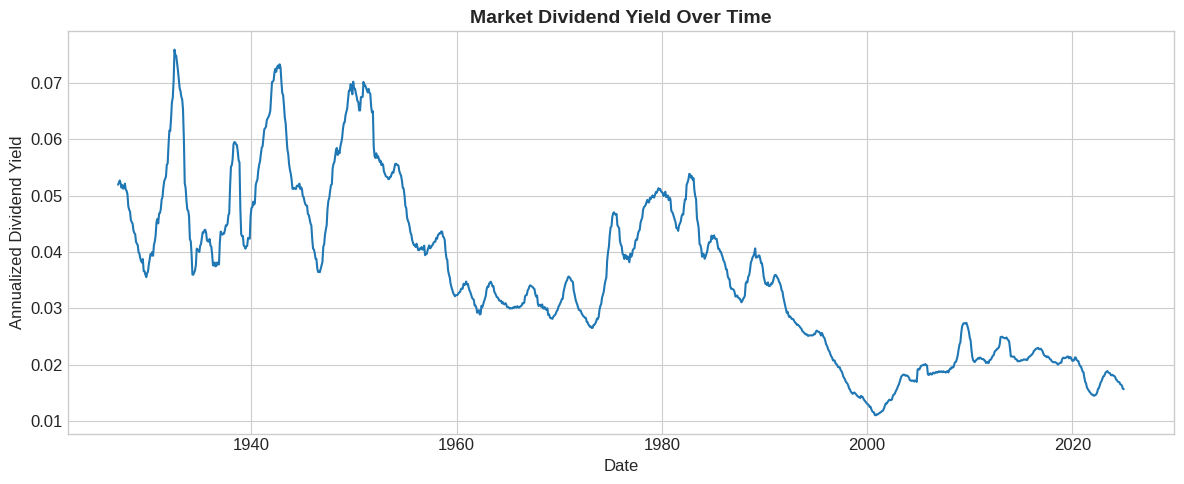

# Plot annualized dividend yield (smoothed over 12 months)

fig, ax = plt.subplots(figsize=(12, 5))

dp_annual = crsp['dp'].rolling(window=12).mean() * 12

ax.plot(dp_annual, linewidth=1.5)

ax.set_xlabel('Date')

ax.set_ylabel('Annualized Dividend Yield')

ax.set_title('Market Dividend Yield Over Time', fontsize=14, fontweight='bold')

plt.tight_layout()

plt.show()

📌 Remember:

Dividend yields ranged from 4-7% in the 1930s to around 2% today.

This secular decline is important for interpretation.

Why ? In english what that means?

🤔 Think:

Why might high dividend yields predict high future returns?

Why might dividend yields NOT predict returns?

5.6.6. Forecasting Regressions #

5.6.6.1. The Forecasting Framework#

To test if a signal predicts returns, run:

Key differences from factor models:

Relationship is not contemporaneous

We know the signal ahead of time

We’re predicting returns over horizon \(h\)

5.6.6.2. Preparing the Data#

# Get risk-free rate

df_factors = get_factors('CAPM', freq='monthly').dropna()

# Align indices

crsp.index = crsp.index + pd.offsets.MonthEnd(0)

# Merge with factors

merged = crsp.merge(df_factors[['RF']], left_index=True, right_index=True)

# Parameters

years = 5 # Forecast horizon

# Compute future 5-year returns (annualized)

merged['R_future'] = (

(1 + merged['vwretd'])

.rolling(window=years * 12)

.apply(np.prod)

.shift(-years * 12) ** (1/years) - 1

)

# Smooth dividend yield (annualized)

merged['dp_avg'] = merged['dp'].rolling(window=12).mean() * 12

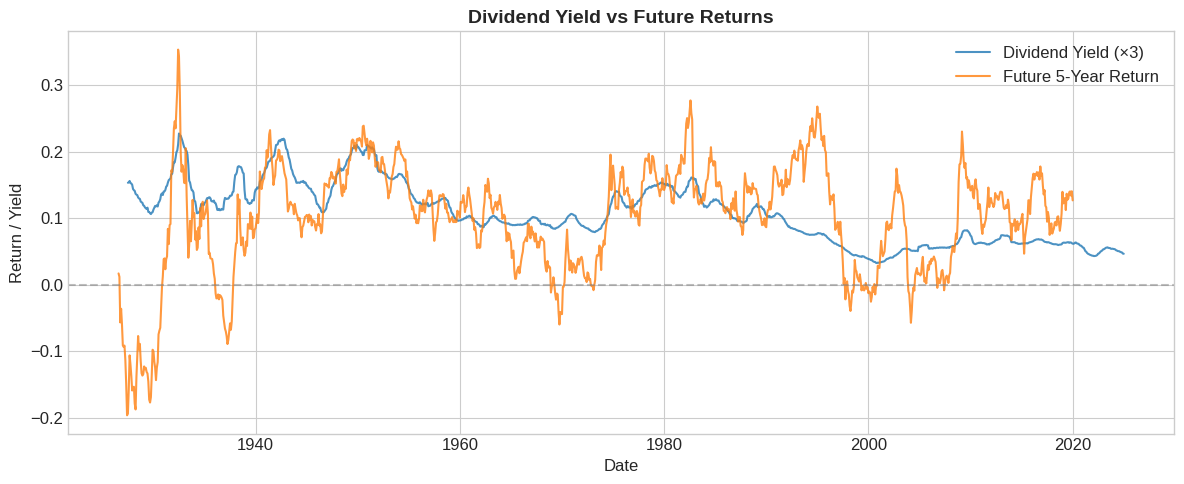

print(f"Correlation: {merged['dp_avg'].corr(merged['R_future']):.3f}")

Correlation: 0.357

# Visualize the relationship

fig, ax = plt.subplots(figsize=(12, 5))

ax.plot(merged.index, merged['dp_avg'] * 3, label='Dividend Yield (×3)', alpha=0.8)

ax.plot(merged.index, merged['R_future'], label='Future 5-Year Return', alpha=0.8)

ax.axhline(0, color='gray', linestyle='--', alpha=0.5)

ax.set_xlabel('Date')

ax.set_ylabel('Return / Yield')

ax.set_title('Dividend Yield vs Future Returns', fontsize=14, fontweight='bold')

ax.legend()

plt.tight_layout()

plt.show()

5.6.6.3. Running the Regression#

# Naive OLS regression

X = sm.add_constant(merged['dp_avg'])

model_naive = sm.OLS(merged['R_future'], X, missing='drop').fit()

print(model_naive.summary())

OLS Regression Results

==============================================================================

Dep. Variable: R_future R-squared: 0.127

Model: OLS Adj. R-squared: 0.127

Method: Least Squares F-statistic: 161.8

Date: Mon, 19 Jan 2026 Prob (F-statistic): 1.08e-34

Time: 18:50:41 Log-Likelihood: 1299.2

No. Observations: 1111 AIC: -2594.

Df Residuals: 1109 BIC: -2584.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0297 0.006 4.878 0.000 0.018 0.042

dp_avg 1.9598 0.154 12.719 0.000 1.657 2.262

==============================================================================

Omnibus: 234.961 Durbin-Watson: 0.044

Prob(Omnibus): 0.000 Jarque-Bera (JB): 563.442

Skew: -1.134 Prob(JB): 4.47e-123

Kurtosis: 5.651 Cond. No. 68.4

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

⚠️ Caution:

Look at that t-statistic! Seems too good to be true…

The problem: overlapping windows inflate the t-statistic. With 5-year returns, consecutive observations share 59 out of 60 months!

5.6.6.4. Correcting for Overlapping Returns#

# HAC standard errors (Newey-West) to correct for overlap

model_hac = sm.OLS(merged['R_future'], X, missing='drop').fit(

cov_type='HAC',

cov_kwds={'maxlags': years * 12}

)

print(model_hac.summary())

OLS Regression Results

==============================================================================

Dep. Variable: R_future R-squared: 0.127

Model: OLS Adj. R-squared: 0.127

Method: Least Squares F-statistic: 11.89

Date: Mon, 19 Jan 2026 Prob (F-statistic): 0.000584

Time: 18:50:46 Log-Likelihood: 1299.2

No. Observations: 1111 AIC: -2594.

Df Residuals: 1109 BIC: -2584.

Df Model: 1

Covariance Type: HAC

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0297 0.024 1.232 0.218 -0.018 0.077

dp_avg 1.9598 0.568 3.449 0.001 0.846 3.074

==============================================================================

Omnibus: 234.961 Durbin-Watson: 0.044

Prob(Omnibus): 0.000 Jarque-Bera (JB): 563.442

Skew: -1.134 Prob(JB): 4.47e-123

Kurtosis: 5.651 Cond. No. 68.4

==============================================================================

Notes:

[1] Standard Errors are heteroscedasticity and autocorrelation robust (HAC) using 60 lags and without small sample correction

💡 Key Insight:

After correcting for overlap, the t-statistic drops substantially. The relationship may still be significant, but with much more uncertainty.

5.6.7. Out-of-Sample Evaluation #

5.6.7.1. Why Out-of-Sample Matters#

We can’t trade on data we haven’t seen yet

Relationships may be spurious or unstable

There are many ways of conducting an out of sample analysis. And there is a lot of science to it

For now we will keep it simple and split in an arbitrary date

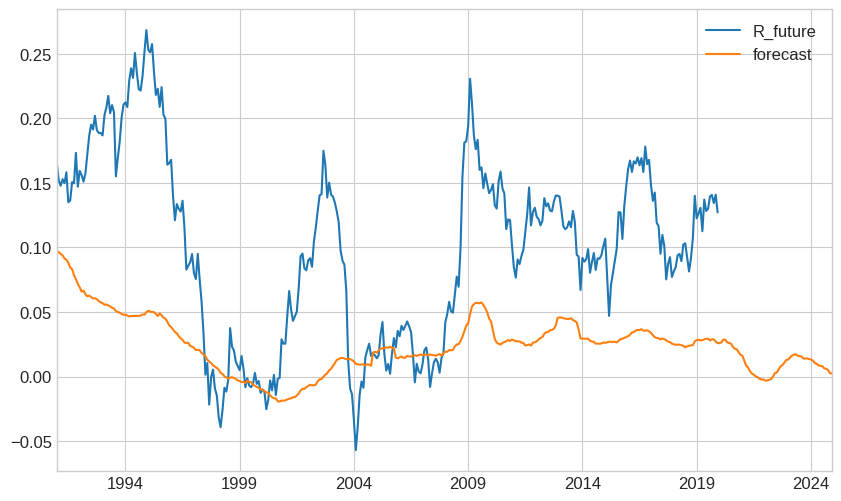

# Split into estimation and test samples

estimation = merged['1950':'1990'].copy()

test = merged['1991':].copy()

# Estimate model on estimation sample

X_est = sm.add_constant(estimation['dp_avg'])

model_est = sm.OLS(estimation['R_future'], X_est, missing='drop').fit(

cov_type='HAC',

cov_kwds={'maxlags': years * 12}

)

# Generate forecasts for test sample USING THE ESTIMATED PARAMETERS IN ESTIMATION SAMPLE

test['forecast'] = model_est.params['const'] + model_est.params['dp_avg'] * test['dp_avg']

test[['R_future','forecast']].plot()

<Axes: >

5.6.7.2. What is going wrong?#

Structural breaks in dividend policy? Firms now returns capital usign buy-backs

Maybe there was a one of reduction in risk-premia and now yields mean-revert around a different average?

but timing the market is very hard

good news is that you can easily test if any suggestion people give makes sense, e.g. Does “Buy the Dip” works?

How to fomally evaluate if it is working?

Form the trading strategy and look at the returns

Out of Sample R-squared

5.6.8. Trading Strategy Implementation #

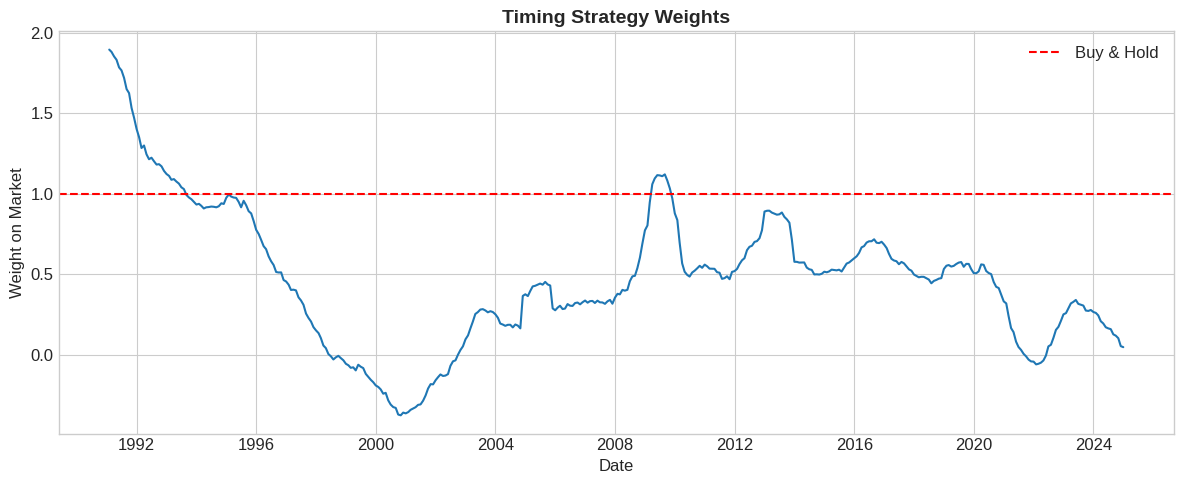

5.6.8.1. From Signal to Weights#

The optimal weight on the market is:

where:

\(\mu_t = a + b \cdot \text{DP}_t\) is the forecasted premium

\(\gamma\) is risk aversion

\(\sigma\) is volatility (assumed constant for now)

# Strategy parameters

gamma = 2

vol = 0.16 # Annual volatility

# Compute weights

test['weight'] = test['forecast'] / (gamma * vol**2)

# Visualize weights

fig, ax = plt.subplots(figsize=(12, 5))

ax.plot(test.index, test['weight'], linewidth=1.5)

ax.axhline(1, color='red', linestyle='--', label='Buy & Hold')

ax.set_xlabel('Date')

ax.set_ylabel('Weight on Market')

ax.set_title('Timing Strategy Weights', fontsize=14, fontweight='bold')

ax.legend()

plt.tight_layout()

plt.show()

5.6.8.2. Strategy Returns#

The timing strategy return is:

test

| vwretd | vwretx | dp | RF_x | R_future | dp_avg | forecast | weight | RF_y | |

|---|---|---|---|---|---|---|---|---|---|

| 1991-01-31 | 0.049083 | 0.046987 | 0.002002 | 0.0052 | 0.117732 | 0.035899 | 0.039267 | 0.766928 | 0.0052 |

| 1991-02-28 | 0.075848 | 0.071836 | 0.003743 | 0.0048 | 0.105225 | 0.035742 | 0.038513 | 0.752212 | 0.0048 |

| 1991-03-31 | 0.028922 | 0.026702 | 0.002162 | 0.0044 | 0.101422 | 0.035436 | 0.037044 | 0.723525 | 0.0044 |

| 1991-04-30 | 0.003311 | 0.001186 | 0.002122 | 0.0053 | 0.106441 | 0.035207 | 0.035950 | 0.702141 | 0.0053 |

| 1991-05-31 | 0.040737 | 0.037177 | 0.003432 | 0.0047 | 0.103558 | 0.034687 | 0.033456 | 0.653443 | 0.0047 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 2024-08-31 | 0.021572 | 0.020203 | 0.001342 | 0.0048 | NaN | 0.016496 | -0.053761 | -1.050016 | 0.0048 |

| 2024-09-30 | 0.020969 | 0.019485 | 0.001456 | 0.0040 | NaN | 0.016407 | -0.054187 | -1.058334 | 0.0040 |

| 2024-10-31 | -0.008298 | -0.009139 | 0.000849 | 0.0039 | NaN | 0.016233 | -0.055020 | -1.074606 | 0.0039 |

| 2024-11-30 | 0.064855 | 0.063463 | 0.001309 | 0.0040 | NaN | 0.015693 | -0.057611 | -1.125224 | 0.0040 |

| 2024-12-31 | -0.031582 | -0.033470 | 0.001953 | 0.0037 | NaN | 0.015622 | -0.057949 | -1.131820 | 0.0037 |

408 rows × 9 columns

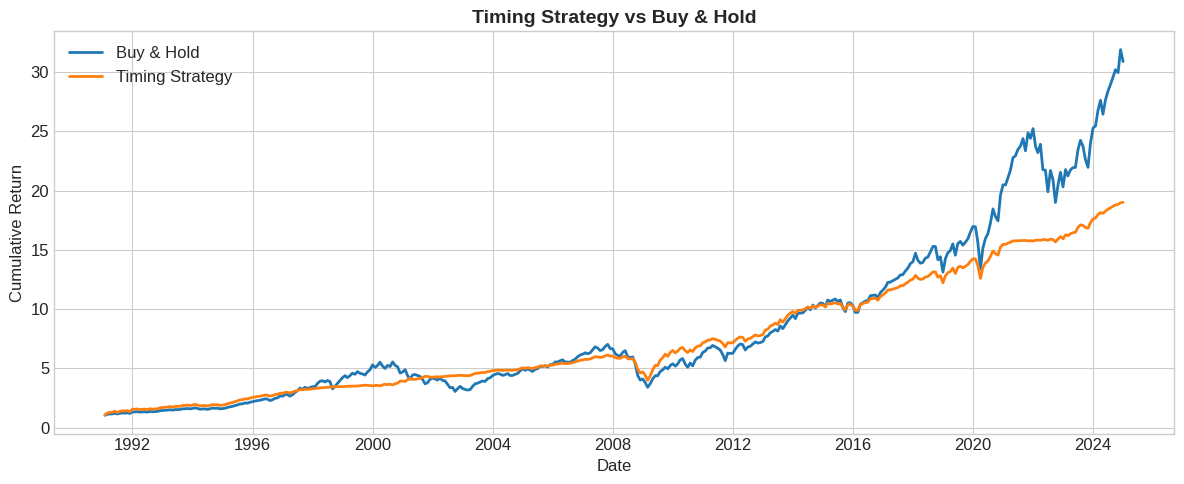

# Merge with factors to get RF

# Compute strategy returns

test['ret_timing'] = test['RF'] + test['weight'] * (test['vwretd'] - test['RF'])

# Cumulative returns

fig, ax = plt.subplots(figsize=(12, 5))

cum_timing = (1 + test['ret_timing']).cumprod()

cum_mkt = (1 + test['vwretd']).cumprod()

ax.plot(test.index, cum_mkt, label='Buy & Hold', linewidth=2)

ax.plot(test.index, cum_timing, label='Timing Strategy', linewidth=2)

ax.set_xlabel('Date')

ax.set_ylabel('Cumulative Return')

ax.set_title('Timing Strategy vs Buy & Hold', fontsize=14, fontweight='bold')

ax.legend()

plt.tight_layout()

plt.show()

5.6.9. Performance Evaluation #

How to evaluate if we “beat the market”?

Is looking at the raw cumulative return enough?

What differences we might want to account for?

5.6.9.2. Out of Sample R-squared#

One thing that people do to evaluate these forecasting regressions is look at the R-squared out of sample relative to some benchmark prediction for the expected returns.

Typically a regression R-squared has the sample average

You compare the model explanatory power, i.e. reduction in \(\sum(r_{t+1}-(a+b *signal_t))^2\), with the reduction in simply subtracting the sample average \(\sum(r_{t+1}-Average(r_{t+1}))^2\)

But we need a bechmark that also cannot see the future–knowign the future average would be amazing right?

what people do is to use the estimation sample average–instead of using the signal–just use past average returns

r_past_average=(estimation['R_future']).mean()

R2_TS=1-((test['R_future']-(test['forecast']))**2).sum()/((test['R_future']-r_past_average)**2).sum()

R2_TS

np.float64(-0.6026909813375205)

How to interpret this negative number?

5.6.10. Exercises #

5.6.10.1. 🔧 Exercise 1: Overlapping Returns Problem#

Explain why overlapping returns cause problems for standard errors.

If we use 5-year returns, how many months overlap between consecutive observations?

What does this do to the effective sample size?

How does HAC correction help?

💡 Click for solution

With 60-month returns, consecutive observations share 59 months of data.

The effective sample size is much smaller than the raw count. If we have 100 years of monthly data (1200 months), we don’t have 1200 independent observations—we have closer to 20 (100/5).

HAC (Heteroskedasticity and Autocorrelation Consistent) standard errors account for the serial correlation induced by overlapping windows, giving us proper inference.

5.6.10.2. 🔧 Exercise 2: Alternative Signals#

Explain the economic intuition for why each signal might predict market returns:

Credit spread (BBB yield - Treasury yield)

VIX (implied volatility index)

Aggregate short interest (fraction of market cap in short positions)

💡 Click for solution

Credit spread: High spreads indicate economic stress and high risk premia. Investors demand more compensation → expect higher future returns.

VIX: High implied volatility may indicate high risk premia (though volatility itself doesn’t predict returns well). The variance risk premium (VIX² - RV) is a better predictor.

Short interest: High short interest may indicate overvaluation or pessimism. If shorts are informed, this predicts lower returns. If it’s excessive pessimism, it could mean mean-reversion (higher returns).

# Your code here

5.6.10.3. 🤔 Exercise 3: Break the Sample#

Using the test sample data:

Split it into two sub-periods of similar size

Compute Sharpe ratios for timing vs buy-and-hold in each sub-period

Are the results stable across periods?

💡 Click for solution

# Split test sample

period1 = test['2011':'2017']

period2 = test['2018':]

for name, df in [('2011-2017', period1), ('2018-2024', period2)]:

sr_t = (df['ret_timing'] - df['RF']).mean() * 12 / ((df['ret_timing'] - df['RF']).std() * np.sqrt(12))

sr_m = (df['vwretd'] - df['RF']).mean() * 12 / ((df['vwretd'] - df['RF']).std() * np.sqrt(12))

print(f"{name}: Timing SR = {sr_t:.3f}, Market SR = {sr_m:.3f}")

Results often vary significantly across periods, highlighting the instability of return predictability.

# Your code here

5.6.11. 📝 Key Takeaways #

To time a factor, you need a signal that predicts future returns. Dividend yield is the classic example, but many others exist.

In-sample predictability is just the start. The relationship must be stable enough to work out-of-sample.

Overlapping returns require special care. Use HAC standard errors or non-overlapping samples for proper inference.

Evaluate with out-of-sample R² or trading strategies. Use the historical average as your benchmark.

The right benchmark has the same average beta. Regress timing returns on the factor and look at alpha.

Dividend yield predictability is weak and unstable. The signal is so persistent that even long samples have few independent observations.

Sharpe ratios isolate timing skill. Pure beta variation is SR-neutral; only alpha improves the Sharpe ratio.