6. Factor Models#

6.1. 🎯 Learning Objectives#

By the end of this notebook, you will be able to:

Decode the α / β decomposition — Split any asset’s excess return into factor-driven and idiosyncratic pieces

Estimate factor exposure with regression — Use OLS to obtain α, β, and residual statistics

Create tracking and hedged portfolios — Build factor-neutral “portable alpha” positions

Apply risk budgets to position sizing — Determine capital allocation under volatility constraints

Evaluate performance with Sharpe and Appraisal ratios — Distinguish skill from factor exposure

6.2. 📋 Table of Contents#

6.3. 🛠️ Setup #

#@title 🛠️ Setup: Run this cell first (click to expand)

# Core libraries

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

%matplotlib inline

# Set consistent plot style

plt.style.use('seaborn-v0_8-whitegrid')

plt.rcParams['figure.figsize'] = [10, 6]

plt.rcParams['font.size'] = 12

# Suppress warnings for cleaner output

import warnings

warnings.filterwarnings('ignore')

print("✅ Libraries loaded successfully!")

✅ Libraries loaded successfully!

#@title Helper Function: Get Factor Data

# pandas-datareader: Fetches financial data from various online sources

# We'll use it to get Fama-French factor data from Ken French's website

import datetime

from pandas_datareader.data import DataReader

def get_factors(factors='CAPM', freq='daily'):

"""Download Fama-French factor data.

Parameters:

- factors: 'CAPM', 'FF3', 'FF5', or 'FF6'

- freq: 'daily' or 'monthly'

Returns: DataFrame with factor returns (as decimals)

"""

freq_label = '' if freq == 'monthly' else '_' + freq

if factors == 'CAPM':

ff = DataReader(f"F-F_Research_Data_Factors{freq_label}", "famafrench", start="1921-01-01")

df_factor = ff[0][['RF', 'Mkt-RF']]

elif factors == 'FF3':

ff = DataReader(f"F-F_Research_Data_Factors{freq_label}", "famafrench", start="1921-01-01")

df_factor = ff[0][['RF', 'Mkt-RF', 'SMB', 'HML']]

elif factors == 'FF5':

ff = DataReader(f"F-F_Research_Data_Factors{freq_label}", "famafrench", start="1921-01-01")

df_factor = ff[0][['RF', 'Mkt-RF', 'SMB', 'HML']]

ff2 = DataReader(f"F-F_Research_Data_5_Factors_2x3{freq_label}", "famafrench", start="1921-01-01")

df_factor = df_factor.merge(ff2[0][['RMW', 'CMA']], on='Date', how='outer')

else: # FF6

ff = DataReader(f"F-F_Research_Data_Factors{freq_label}", "famafrench", start="1921-01-01")

df_factor = ff[0][['RF', 'Mkt-RF', 'SMB', 'HML']]

ff2 = DataReader(f"F-F_Research_Data_5_Factors_2x3{freq_label}", "famafrench", start="1921-01-01")

df_factor = df_factor.merge(ff2[0][['RMW', 'CMA']], on='Date', how='outer')

ff_mom = DataReader(f"F-F_Momentum_Factor{freq_label}", "famafrench", start="1921-01-01")

df_factor = df_factor.merge(ff_mom[0], on='Date')

df_factor.columns = ['RF', 'Mkt-RF', 'SMB', 'HML', 'RMW', 'CMA', 'MOM']

if freq == 'monthly':

df_factor.index = pd.to_datetime(df_factor.index.to_timestamp()) + pd.offsets.MonthEnd(0)

else:

df_factor.index = pd.to_datetime(df_factor.index)

return df_factor / 100 # Convert from percent to decimal

6.3.1. Loading Return Data#

# Load excess returns for SPY, WMT, JPM

url = 'https://raw.githubusercontent.com/amoreira2/UG54/refs/heads/main/assets/data/FactorModels_data1.csv'

df_re = pd.read_csv(url, parse_dates=['date'], index_col='date')

print(f"Data range: {df_re.index.min().date()} to {df_re.index.max().date()}")

print(f"Stocks: {list(df_re.columns)}")

# Prepare data (drop missing values)

data = df_re.dropna()

data.tail()

Data range: 1969-03-05 to 2024-12-31

Stocks: ['SPY', 'WMT', 'JPM']

| SPY | WMT | JPM | |

|---|---|---|---|

| date | |||

| 2024-12-24 | 0.010940 | 0.025614 | 0.016269 |

| 2024-12-26 | -0.000106 | 0.001014 | 0.003252 |

| 2024-12-27 | -0.010698 | -0.012349 | -0.008273 |

| 2024-12-30 | -0.011585 | -0.012065 | -0.007844 |

| 2024-12-31 | -0.003811 | -0.002602 | 0.001457 |

6.4. Co-movement #

6.4.1. The Core Insight#

To understand how much to invest in different stocks, the first step is to understand to what extent stocks are alike and to what extent they are different.

It makes no sense to say tht you are buying to buy a bunch of different assets to be diversified if they all behave alike each other

Stocks don’t move independently—they co-move with the market.

But the degree of co-movement varies:

Defensive stocks (utilities, groceries) → less sensitive to market swings

Cyclical stocks (luxury goods, banks) → more sensitive to market swings

High-leverage stocks → particularly vulnerable in downturns

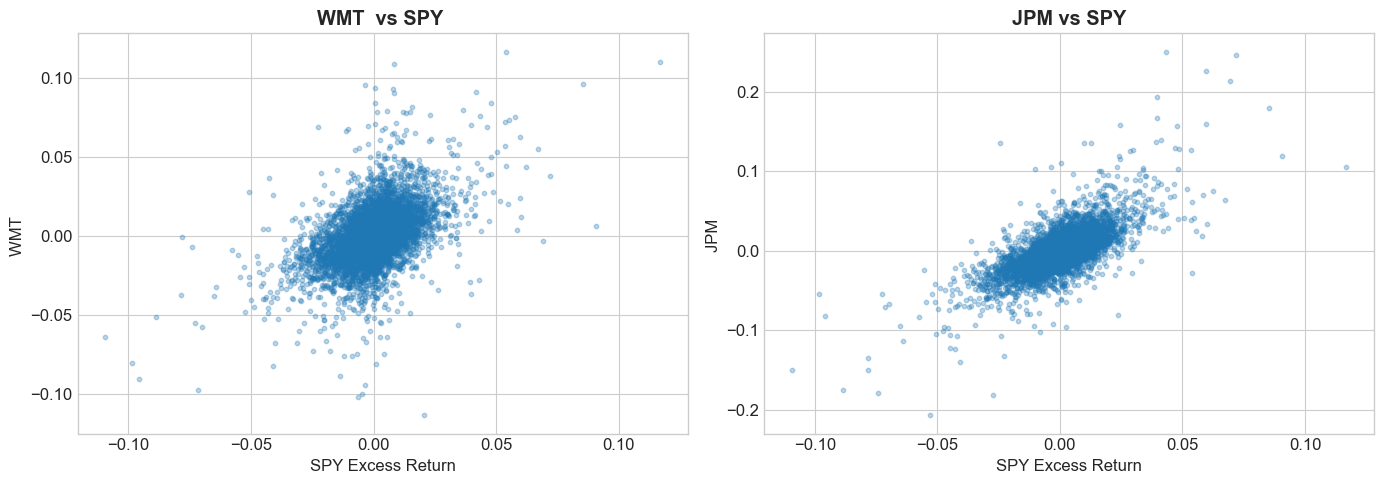

6.4.2. Visualizing Co-movement#

# Create residuals

wmt = data['WMT']

jpm = data['JPM']

# Plot residuals vs factor

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

axes[0].scatter(data['SPY'], wmt, alpha=0.3, s=10)

axes[0].set_xlabel('SPY Excess Return')

axes[0].set_ylabel('WMT ')

axes[0].set_title(f'WMT vs SPY ', fontweight='bold')

axes[1].scatter(data['SPY'], jpm, alpha=0.3, s=10)

axes[1].set_xlabel('SPY Excess Return')

axes[1].set_ylabel('JPM ')

axes[1].set_title(f'JPM vs SPY', fontweight='bold')

plt.tight_layout()

plt.show()

6.4.3. Towards a Factor Model#

We decompose any asset’s excess return as:

Where:

\(r^e\) = asset’s excess return over risk-free rate

\(\alpha\) = intercept (skill/mispricing)

\(\beta\) = sensitivity to factor

\(f\) = factor excess return (e.g., market)

\(\epsilon\) = idiosyncratic (asset-specific) risk

💡 Key Insight:

This decomposition is always valid—it’s just statistics. The power comes from interpreting each piece:

\(\beta \cdot f\) is the return you could get by investing in the factor in a way that tracks the asset as well as possible

\(\alpha+\epsilon\) is the return specific to the asset only. Alpha is the mean. Epsilon is the noise.

🤔 Think and Code:

How do we estimate \(\beta\) and \(\alpha\) from data?

What should we plot to visualize if the factor model “works”?

What do you expect the correlation between residuals and factor to be?

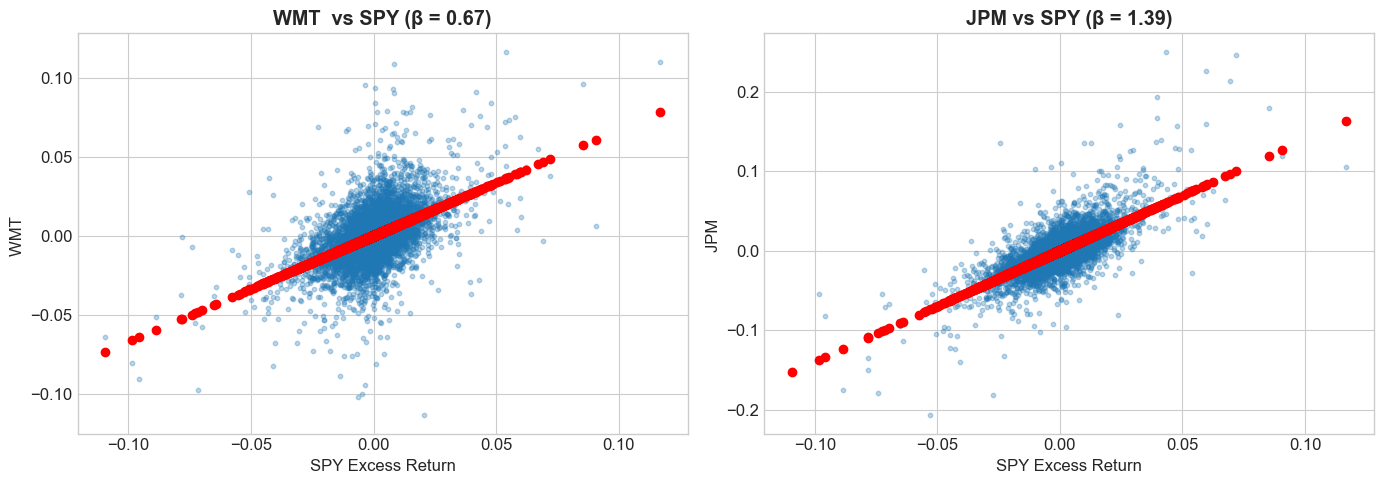

6.4.4. Estimating Beta with Regression#

# statsmodels: Statistical modeling library for Python

# Provides OLS regression, hypothesis testing, and model diagnostics

import statsmodels.formula.api as smf

# Run regressions for WMT and JPM on SPY

model_wmt = smf.ols(formula='WMT ~ SPY', data=data).fit()

model_jpm = smf.ols(formula='JPM ~ SPY', data=data).fit()

alpha_wmt, beta_wmt = model_wmt.params

alpha_jpm, beta_jpm = model_jpm.params

print(f"WMT: α = {alpha_wmt:.6f}, β = {beta_wmt:.3f}")

print(f"JPM: α = {alpha_jpm:.6f}, β = {beta_jpm:.3f}")

WMT: α = 0.000203, β = 0.674

JPM: α = 0.000159, β = 1.395

📌 Remember:

\(\beta < 1\): Less sensitive than market (defensive)

\(\beta = 1\): Same sensitivity as market

\(\beta > 1\): More sensitive than market (aggressive)

6.4.5. Visualizing Co-movement#

# Create residuals

wmt = data['WMT']

jpm = data['JPM']

# Plot residuals vs factor

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

axes[0].scatter(data['SPY'], wmt, alpha=0.3, s=10)

axes[0].scatter(data['SPY'],alpha_wmt+beta_wmt * data['SPY'], color='red', linestyle='-')

axes[0].set_xlabel('SPY Excess Return')

axes[0].set_ylabel('WMT ')

axes[0].set_title(f'WMT vs SPY (β = {beta_wmt:.2f})', fontweight='bold')

axes[1].scatter(data['SPY'], jpm, alpha=0.3, s=10)

axes[1].scatter(data['SPY'],alpha_jpm+beta_jpm * data['SPY'], color='red', linestyle='-')

axes[1].set_xlabel('SPY Excess Return')

axes[1].set_ylabel('JPM ')

axes[1].set_title(f'JPM vs SPY (β = {beta_jpm:.2f})', fontweight='bold')

plt.tight_layout()

plt.show()

# Verify residuals are uncorrelated with factor

print(f"Correlation of SPY with WMT : {data['SPY'].corr(wmt):.6f}")

print(f"Correlation of SPY with JPM: {data['SPY'].corr(jpm):.6f}")

Correlation of SPY with WMT : 0.492221

Correlation of SPY with JPM: 0.707302

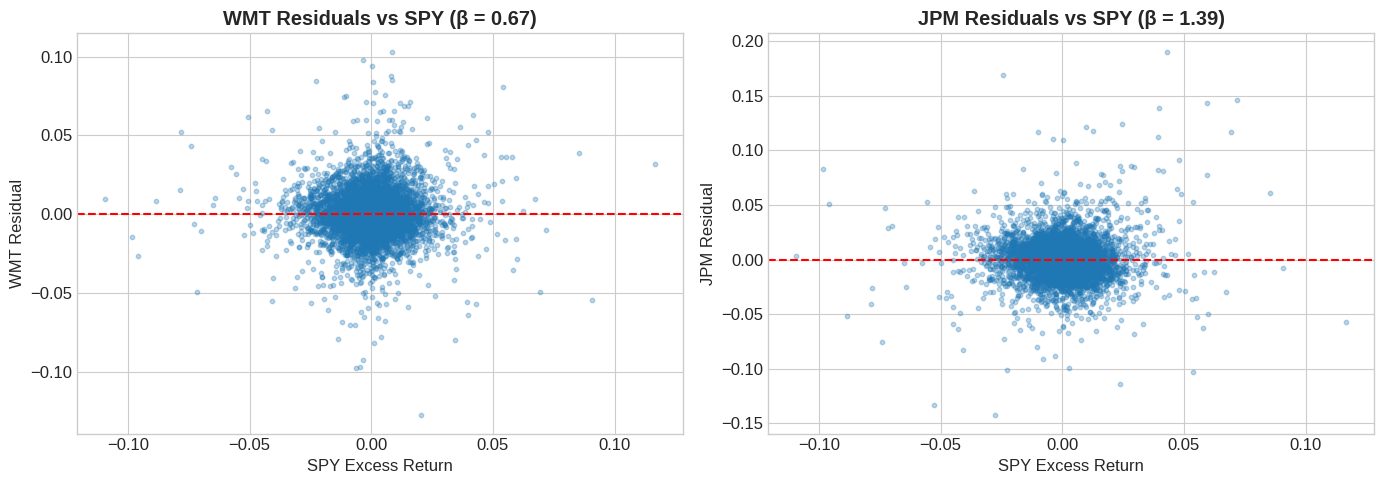

# Create residuals

resid_wmt = data['WMT'] - beta_wmt * data['SPY']

resid_jpm = data['JPM'] - beta_jpm * data['SPY']

# Plot residuals vs factor

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

axes[0].scatter(data['SPY'], resid_wmt, alpha=0.3, s=10)

axes[0].axhline(0, color='red', linestyle='--')

axes[0].set_xlabel('SPY Excess Return')

axes[0].set_ylabel('WMT Residual')

axes[0].set_title(f'WMT Residuals vs SPY (β = {beta_wmt:.2f})', fontweight='bold')

axes[1].scatter(data['SPY'], resid_jpm, alpha=0.3, s=10)

axes[1].axhline(0, color='red', linestyle='--')

axes[1].set_xlabel('SPY Excess Return')

axes[1].set_ylabel('JPM Residual')

axes[1].set_title(f'JPM Residuals vs SPY (β = {beta_jpm:.2f})', fontweight='bold')

plt.tight_layout()

plt.show()

# Verify residuals are uncorrelated with factor

print(f"Correlation of SPY with WMT residuals: {data['SPY'].corr(resid_wmt):.6f}")

print(f"Correlation of SPY with JPM residuals: {data['SPY'].corr(resid_jpm):.6f}")

Correlation of SPY with WMT residuals: 0.000000

Correlation of SPY with JPM residuals: 0.000000

6.5. Risk Models vs Expected Return Models #

Factor models serve two distinct purposes:

6.5.1. 👉 Risk Models#

Goal: Explain realized return variation

Assumption: \(\epsilon\) is uncorrelated across assets

Key metric: R-squared (how much variance is explained?)

Can it explain realized returns?

Use case: Risk management, covariance estimation

6.5.2. 👉 Expected Return Models#

Goal: Explain expected return differences

Assumption: \(\alpha = 0\) for all assets

Key metric: Alpha (is it close to zero?)

can it explain differences in Average returns across assets and strategies as a function of factor loadings (i.e. betas?)

Use case: Performance evaluation, asset pricing tests

💡 Key Insight:

A model can be great for risk but poor for expected returns. For stocks, factor models explain lots of variance but still leave substantial uncertainty about expected returns.

6.6. Alpha and Beta: The Organization of Wall Street #

6.6.1. How the Industry is Organized#

The \(\alpha\)- \(\beta\) decomposition is how Wall Street operates:

Big bonuses only come from perceied \(\alpha\) (skill)

Beta exposure is close to a commodity—exact commodity for market exposure, closer to commodity for other factors

Pod shops require traders to be factor-neutral (not only market but across many factors):

6.6.2. From Factor Exposure to Expected Returns#

Taking expectations of our factor model:

Expected return decomposes into:

\(r_f\): Risk-free rate (time value of money)

\(\beta \cdot E[f]\): Premium from factor exposure

\(\alpha\): Abnormal return (skill or mispricing)

⚠️ Caution:

If you have a good model of expected returns, \(\alpha\) should be zero. A significant \(\alpha\) means either:

You found skill/mispricing, OR

Your factor model is missing something

So it is all about interepretation.

In the industry, a trader often takes the factor model as given and try to beat it

The factor model can come from clients or the central book.

If you are a family office, managing money for a sovereign wealth fund, or giving advice to a client it will be your job to determine what factors to include

6.7. Tracking and Hedged Portfolios #

6.7.1. Loading MSFT Data for Hedging Example#

# Load MSFT returns

url_msft = 'https://raw.githubusercontent.com/amoreira2/UG54/refs/heads/main/assets/data/FactorModels_data2.csv'

df_returns = pd.read_csv(url_msft, parse_dates=['date'], index_col='date')

# Get factor data

df_factor = get_factors()

# Align the two DataFrames on common dates

df_returns, df_factor = df_returns.dropna().align(df_factor.dropna(), join='inner', axis=0)

print(f"Data range: {df_returns.index.min().date()} to {df_returns.index.max().date()}")

print(f"Observations: {len(df_returns)}")

Data range: 1986-03-14 to 2024-12-31

Observations: 9778

6.7.2. Running the Factor Regression#

import statsmodels.api as sm

# Compute MSFT excess returns

df_eret = df_returns['MSFT'] - df_factor['RF']

# Prepare regression

X = sm.add_constant(df_factor['Mkt-RF']) # Add intercept

y = df_eret

# Fit OLS model

model = sm.OLS(y, X).fit()

print(model.summary())

OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.415

Model: OLS Adj. R-squared: 0.415

Method: Least Squares F-statistic: 6940.

Date: Wed, 04 Feb 2026 Prob (F-statistic): 0.00

Time: 14:10:18 Log-Likelihood: 26516.

No. Observations: 9778 AIC: -5.303e+04

Df Residuals: 9776 BIC: -5.301e+04

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 0.0006 0.000 3.597 0.000 0.000 0.001

Mkt-RF 1.1876 0.014 83.309 0.000 1.160 1.216

==============================================================================

Omnibus: 1452.828 Durbin-Watson: 1.929

Prob(Omnibus): 0.000 Jarque-Bera (JB): 22202.613

Skew: 0.141 Prob(JB): 0.00

Kurtosis: 10.377 Cond. No. 87.7

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

6.7.3. Magnitudes#

🤔 Think and Code:

Is this alpha economically significant?

What shoudl I do to have a sense of it?

IS it a good bet on a risk-reward sense? What should I look at?

# Extract key statistics

alpha = model.params['const']

beta = model.params['Mkt-RF']

var_r = y.var()

var_f = df_factor['Mkt-RF'].var()

var_e = model.resid.var()

mu_f = df_factor['Mkt-RF'].mean()

print(f"Alpha : {alpha:.6f}")

print(f"Beta: {beta:.3f}")

print(f"Variance of MSFT: {var_r:.6f}")

print(f"Variance of MKT: {var_f:.6f}")

print(f"Variance of resid: {var_e:.6f}")

print(f"Mean MKT excess: {mu_f:.6f}")

Alpha : 0.000585

Beta: 1.188

Variance of MSFT: 0.000442

Variance of MKT: 0.000130

Variance of resid: 0.000258

Mean MKT excess: 0.000359

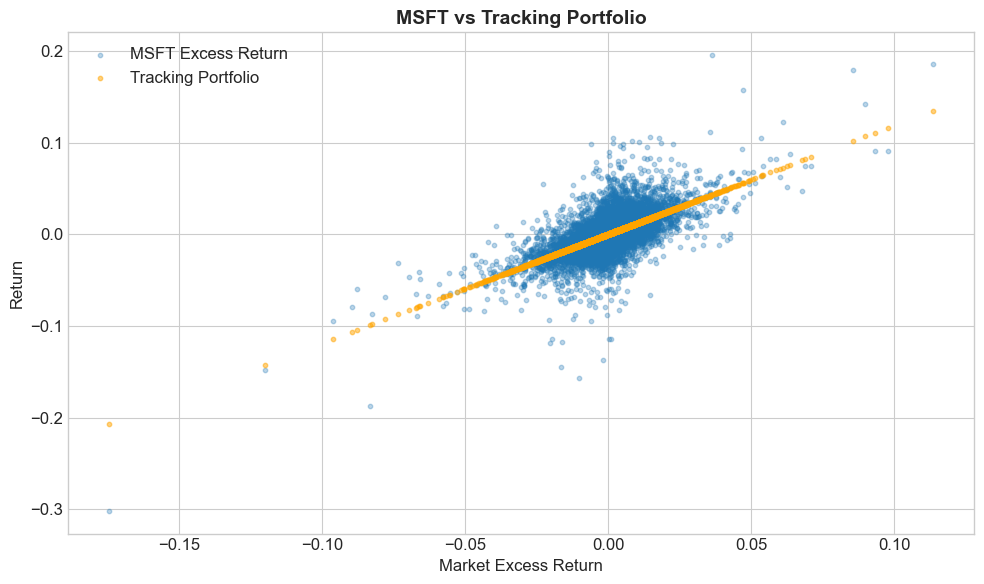

6.7.4. The Tracking Portfolio (also called mimicking portfolio, factor-mimicking portfolio or Hedging Portfolio)#

The tracking portfolio replicates the factor-driven component:

For MSFT with \(\beta \approx 1.2\):

For every 1 dollar in MSFT, hold \(\beta\) dollars in the market factor

# Compute tracking portfolio returns

MKT = df_factor['Mkt-RF']

Portfolio = df_eret

Tracking = MKT * beta

# Plot actual vs tracking

fig, ax = plt.subplots(figsize=(10, 6))

ax.scatter(MKT, Portfolio, alpha=0.3, s=10, label='MSFT Excess Return')

ax.scatter(MKT, Tracking, alpha=0.5, s=10, label='Tracking Portfolio', color='orange')

ax.set_xlabel('Market Excess Return')

ax.set_ylabel('Return')

ax.set_title('MSFT vs Tracking Portfolio', fontsize=14, fontweight='bold')

ax.legend()

plt.tight_layout()

plt.show()

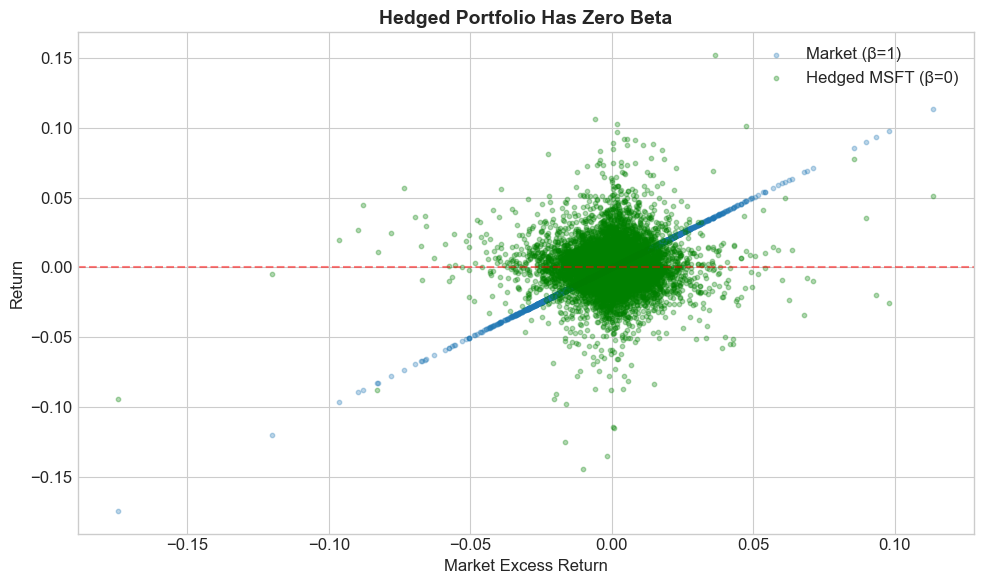

6.7.5. The Hedged Portfolio#

The hedged portfolio removes all factor exposure:

Properties:

Mean return = \(\alpha\) (pure skill)

Volatility = \(\sigma_{\epsilon}\) (only idiosyncratic risk), often that is the compoentn that people call Tracking error

Beta = 0 (by construction, we already stripped out all factor exposure!)

# Compute hedged portfolio

Hedged = Portfolio - Tracking

# Visualize

fig, ax = plt.subplots(figsize=(10, 6))

ax.scatter(MKT, MKT, alpha=0.3, s=10, label='Market (β=1)')

ax.scatter(MKT, Hedged, alpha=0.3, s=10, label='Hedged MSFT (β=0)', color='green')

ax.axhline(0, color='red', linestyle='--', alpha=0.5)

ax.set_xlabel('Market Excess Return')

ax.set_ylabel('Return')

ax.set_title('Hedged Portfolio Has Zero Beta', fontsize=14, fontweight='bold')

ax.legend()

plt.tight_layout()

plt.show()

# Verify

print(f"Hedged portfolio mean (annualized): {Hedged.mean() * 252:.4f}")

print(f"Alpha (annualized): {alpha * 252:.4f}")

Hedged portfolio mean (annualized): 0.1474

Alpha (annualized): 0.1474

6.8. Risk Budgets and Position Sizing #

6.8.1. Position Sizing Under a Volatility Budget#

Suppose you have a $1 million/month volatility budget.

How much MSFT can you buy?

What is the math?

# Monthly volatility of MSFT

vol_monthly = np.sqrt(var_r) * np.sqrt(21) # ~21 trading days per month

# Volatility budget

budget = 1_000_000 # $1M

# Position size

x = ____

print(f"MSFT monthly volatility: {vol_monthly:.4f}")

print(f"Position size: ${x:,.0f}")

---------------------------------------------------------------------------

NameError Traceback (most recent call last)

Cell In[17], line 8

5 budget = 1_000_000 # $1M

7 # Position size

----> 8 x = ____

10 print(f"MSFT monthly volatility: {vol_monthly:.4f}")

11 print(f"Position size: ${x:,.0f}")

NameError: name '____' is not defined

6.8.2. Expected P&L#

Your expected P&L has two components:

Total: \(x \times (\beta \cdot \mu_f + \alpha) \times 252\)

Risk-adjusted: \(x \times \alpha \times 252\) (what you get paid for)

print(f"Expected annual P&L (total): ${x * (beta * mu_f + alpha) * 252:,.0f}")

print(f"Expected annual P&L (risk-adjusted): ${x * alpha * 252:,.0f}")

Expected annual P&L (total): $2,644,594

Expected annual P&L (risk-adjusted): $1,530,371

6.8.3. Hedging Allows Larger Positions#

With hedging, volatility = \(\sigma_\epsilon\) (smaller than \(\sigma_r\)).

You can take a larger position for the same risk budget!

# Hedged volatility (annual)

vol_hedged_annual = np.sqrt(var_e) * np.sqrt(21)

# Annual budget

budget_annual = 1_000_000

# Hedged position size

xe = budget_annual / vol_hedged_annual

print(f"Unhedged vol (annual): {np.sqrt(var_r) * np.sqrt(252):.4f}")

print(f"Hedged vol (annual): {vol_hedged_annual:.4f}")

print(f"\nUnhedged position: ${x}")

print(f"Hedged position: ${xe}")

print(f"\nHedged P&L: ${xe * alpha * 252:,.0f}")

Unhedged vol (annual): 0.3336

Hedged vol (annual): 0.0736

---------------------------------------------------------------------------

NameError Traceback (most recent call last)

Cell In[18], line 12

10 print(f"Unhedged vol (annual): {np.sqrt(var_r) * np.sqrt(252):.4f}")

11 print(f"Hedged vol (annual): {vol_hedged_annual:.4f}")

---> 12 print(f"\nUnhedged position: ${x:,.0f}")

13 print(f"Hedged position: ${xe:,.0f}")

14 print(f"\nHedged P&L: ${xe * alpha * 252:,.0f}")

NameError: name 'x' is not defined

💡 Key Insight:

Hedging reduces volatility, which allows larger position sizes. If your alpha is genuine, hedging lets you earn more of it!

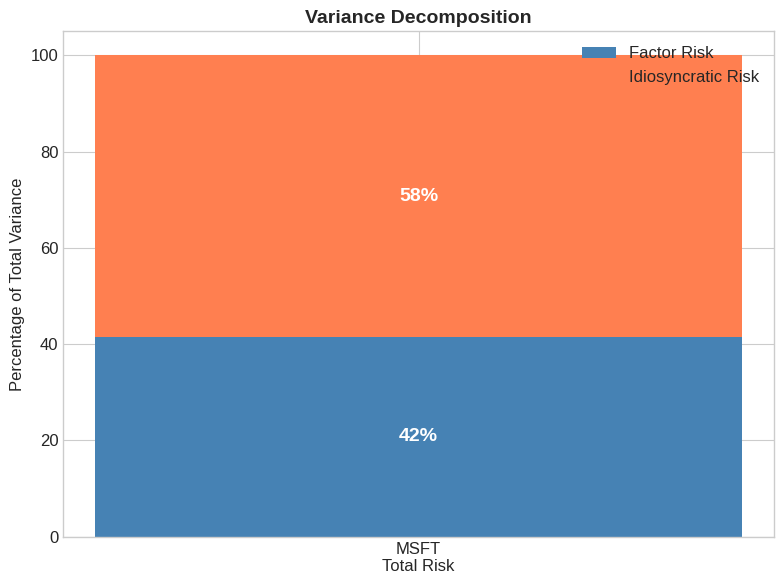

6.10. Variance Decomposition #

6.10.1. Breaking Down Total Risk#

Total variance decomposes into factor and idiosyncratic parts:

The factor risk share is:

# Variance decomposition

factor_var = beta**2 * var_f

idio_var = var_e

total_var = var_r

factor_share = factor_var / total_var

idio_share = idio_var / total_var

print(f"Factor variance contribution: {factor_var:.6f} ({factor_share:.1%})")

print(f"Idiosyncratic variance: {idio_var:.6f} ({idio_share:.1%})")

print(f"Total variance: {total_var:.6f}")

# This should equal R-squared

print(f"\nR-squared from regression: {model.rsquared:.3f}")

print(f"Factor share: {factor_share:.3f}")

Factor variance contribution: 0.000183 (41.5%)

Idiosyncratic variance: 0.000258 (58.5%)

Total variance: 0.000442

R-squared from regression: 0.415

Factor share: 0.415

# Visualize variance decomposition

fig, ax = plt.subplots(figsize=(8, 6))

categories = ['MSFT\nTotal Risk']

factor_vals = [factor_share * 100]

idio_vals = [idio_share * 100]

ax.bar(categories, factor_vals, label='Factor Risk', color='steelblue')

ax.bar(categories, idio_vals, bottom=factor_vals, label='Idiosyncratic Risk', color='coral')

ax.set_ylabel('Percentage of Total Variance')

ax.set_title('Variance Decomposition', fontsize=14, fontweight='bold')

ax.legend()

ax.set_ylim(0, 105)

# Add percentage labels

ax.text(0, factor_share * 50, f'{factor_share:.0%}', ha='center', va='center',

fontsize=14, fontweight='bold', color='white')

ax.text(0, factor_share * 100 + idio_share * 50, f'{idio_share:.0%}', ha='center',

va='center', fontsize=14, fontweight='bold', color='white')

plt.tight_layout()

plt.show()

6.11. Exercises #

6.11.1. 🔧 Exercise 1: Estimate Factor Model for JPM#

Using the df_re DataFrame loaded earlier:

Run a regression of JPM excess returns on SPY

Report the \(\alpha\), \(\beta\), and R-squared

Is JPM more or less sensitive to the market than WMT?

💡 Click for solution

import statsmodels.api as sm

# Prepare data

data = df_re.dropna()

X = sm.add_constant(data['SPY'])

y = data['JPM']

# Fit model

model_jpm = sm.OLS(y, X).fit()

print(f"Alpha: {model_jpm.params['const']:.6f}")

print(f"Beta: {model_jpm.params['SPY']:.3f}")

print(f"R-squared: {model_jpm.rsquared:.3f}")

JPM has a higher beta than WMT, making it more sensitive to market movements.

# Your code here

6.11.2. 🔧 Exercise 2: Build a Hedged Portfolio#

Using your JPM regression results:

Compute the hedged portfolio returns: \(r^{\text{hedged}} = r^e_{JPM} - \beta \times r^e_{SPY}\)

Verify that the hedged portfolio has zero correlation with SPY

Calculate the Sharpe ratio of the hedged vs unhedged portfolio

💡 Click for solution

beta_jpm = model_jpm.params['SPY']

# Hedged portfolio

hedged_jpm = data['JPM'] - beta_jpm * data['SPY']

# Verify zero correlation

print(f"Correlation with SPY: {data['SPY'].corr(hedged_jpm):.6f}")

# Sharpe ratios

sharpe_unhedged = (data['JPM'].mean() * 252) / (data['JPM'].std() * np.sqrt(252))

sharpe_hedged = (hedged_jpm.mean() * 252) / (hedged_jpm.std() * np.sqrt(252))

print(f"Sharpe (unhedged): {sharpe_unhedged:.3f}")

print(f"Sharpe (hedged): {sharpe_hedged:.3f}")

# Your code here

6.11.3. 🤔 Exercise 3: Position Sizing Challenge#

You have a $5 million annual volatility budget.

How much can you invest in JPM (unhedged)?

How much can you invest in the hedged JPM strategy?

What is the expected risk-adjusted P&L for each?

💡 Click for solution

budget = 5_000_000

# Volatilities

vol_jpm = data['JPM'].std() * np.sqrt(252)

vol_hedged = hedged_jpm.std() * np.sqrt(252)

# Position sizes

pos_unhedged = budget / vol_jpm

pos_hedged = budget / vol_hedged

print(f"Unhedged position: ${pos_unhedged:,.0f}")

print(f"Hedged position: ${pos_hedged:,.0f}")

# Risk-adjusted P&L (alpha only)

alpha_jpm = model_jpm.params['const']

pnl_unhedged = pos_unhedged * alpha_jpm * 252

pnl_hedged = pos_hedged * alpha_jpm * 252

print(f"\nRisk-adjusted P&L (unhedged): ${pnl_unhedged:,.0f}")

print(f"Risk-adjusted P&L (hedged): ${pnl_hedged:,.0f}")

# Your code here

6.12. 📝 Key Takeaways #

Factor models separate what you earn from what you ride. Beta captures common market movements; alpha is the slice of return not explained by those movements.

Hedging out β turns views into “portable” alpha. Going long the asset and short β units of the factor neutralizes systematic risk.

Risk budgets shrink once you hedge intelligently. A hedged position’s lower volatility allows you to deploy more capital for the same risk cap.

Variance decomposition is your monitoring dashboard. It tells you how much of today’s risk is coming from factors versus idiosyncratic shocks.

Tracking portfolios clarify performance attribution. By explicitly matching the factor component, you can assess whether outperformance is genuine skill or hidden beta.

All numbers are frequency-specific. Alpha, variances, and Sharpe ratios must be annualized consistently. Beta is theoretically invariant to frequency.