To Be Done

import numpy as np

import pandas as pd

%matplotlib inline

import matplotlib.pyplot as plt

import statsmodels.api as sm

C:\Users\alan.moreira\AppData\Roaming\Python\Python39\site-packages\pandas\core\computation\expressions.py:21: UserWarning: Pandas requires version '2.8.4' or newer of 'numexpr' (version '2.8.1' currently installed).

from pandas.core.computation.check import NUMEXPR_INSTALLED

C:\Users\alan.moreira\AppData\Roaming\Python\Python39\site-packages\pandas\core\arrays\masked.py:60: UserWarning: Pandas requires version '1.3.6' or newer of 'bottleneck' (version '1.3.4' currently installed).

from pandas.core import (

15. Trading costs and Liquidity#

So we have taken prices as given and discussed quantitative allocation rules that overperform relative to a standard CAPM benchmark.

An important question is whether we would be able to trade at those prices if we tried to implement the strategy.

Liquidity is the ease of trading a security.

This encompass many factors, all of which impose a cost on those wishing to trade.

Sources of illiquidity:

Exogenous transactions costs = brokerage fees, order-processing costs, transaction taxes.

Demand pressure = when need to sell quickly, nautral buyer not available. Whoever is available will ask to be compensated to absorb the trade

Inventory risk = if can’t find a buyer will sell to a market maker who will later sell position. But, since market maker faces future price changes, he might demand compensation for this risk

Private information = concern over trading against an informed party (e.g., insider). Need to be compensated for this risk. Private information can be about fundamentals or about future flows.

Obviuosly a perfect answer to this question requires costly experimentation. It would require trading and measuring how prices change in reponse to your trading behavior.

15.1. Implementation Shortfall#

Wish portfolio: your portfolio is trading costs were zero

Performance of wish portfolio: compute returns in real time assuming you can trade at the mid

Shortfall=return of wish portfolio- return of real portfolio

(after all costs)

Shortfall includes both execution costs ( the costs of trading to get you to the wish portfolio) and opportunity costs ( the costs of deviating from the wish portfolio )

IF you trade quickly what force will increase the Shotfall ?Which will increase?

How should you trade in this world?

Precise answer is highly empirical

But overall shape of the solution is clear

Find size of tracking error that minimize shortfall

IF your weights imply a tracking below the cap, don;t trade

Trade whenever tracking error going above this value

Trade just enough to keep tracking error at the cap

Key for this trade-off is the cost of trading.

Trading cost highly dependent of who is trading

Why?

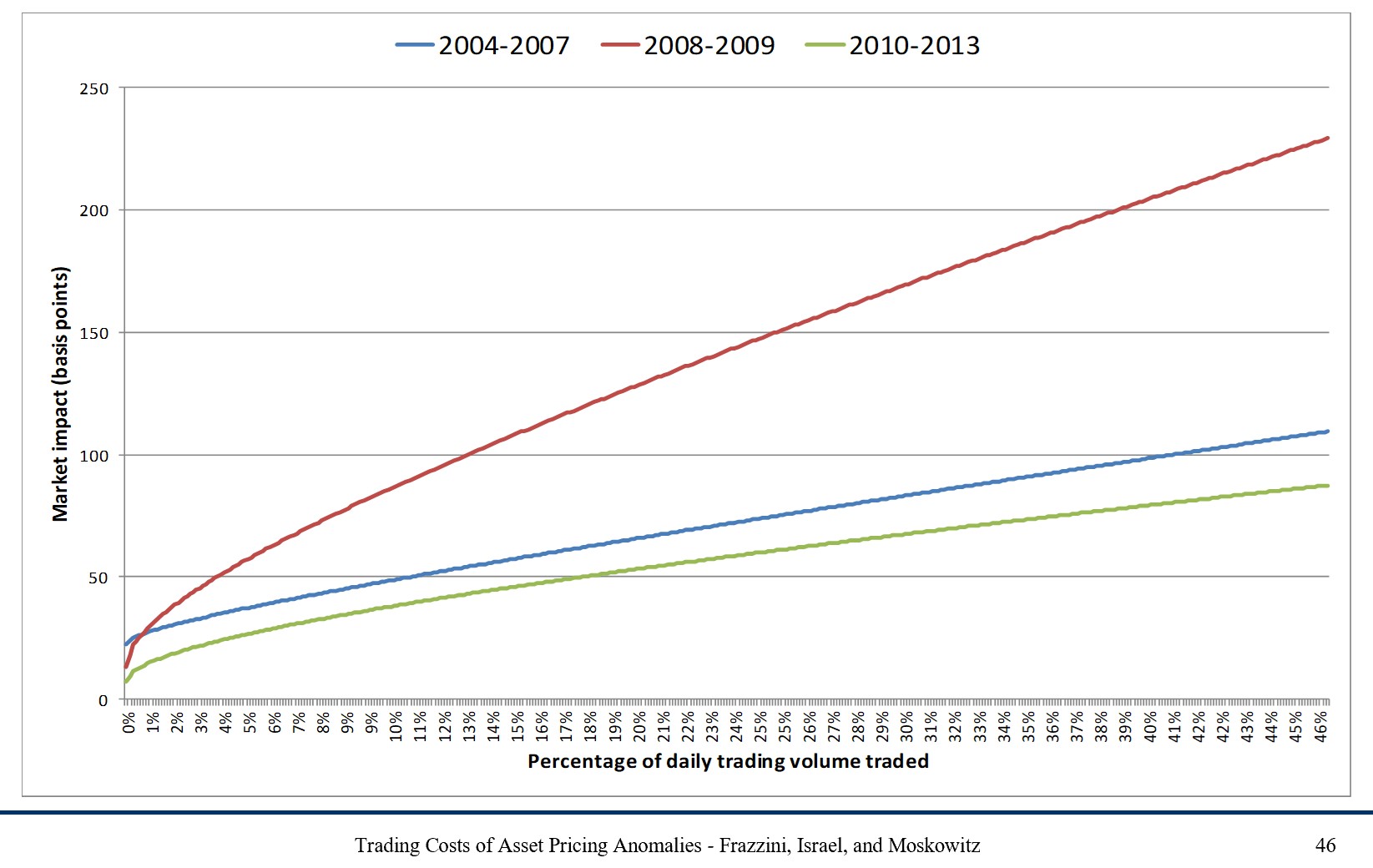

15.2. Absorption capacity#

The idea is to measure how much of the trading volume of each stock you would “use” to implement the strategy for a given position size

Specifically:

The idea is that if you trade a small share of the volume, you are likely to be able to trade at the posted prices.

This graph below shows costs for Trades made by AQR

15.3. How much do you actually need to trade?#

To compute how much you need to trade you need to compare the desired weights in date \(t\) with the weights you have in the end of date \(t+1\).

Before trading, your weight in date \(t+1\) is

If the desired position in the stock is \(w_{i,t+1}^*\), then $\( \begin{align} UsedVolume_{i,t}&=\frac{position \times \bigg(w_{i,t+1}^*-w_{i,t+1}(\text{before trading})\bigg)}{Volume_{i,t}} \\ &=\frac{position}{Volume_{i,t}}\left(w_{i,t+1}^*-\frac{w_{i,t}^*(1+r_{i,t+1})}{1+r_{t+1}^{strategy}}\right) \end{align}\)$

\(UsedVolume_{i,t}\) is a stock-time specific statistic. Implementability will depend on how high this quantity is across time and across stocks– the lower the better.

If it is very high (i.e., close to 1), it means that your position would require almost all volume in a particular stock. It doesn’t mean that you wouldn’t be able to trade, but likely prices would move against you (i.e., go up as you buy, do down as you sell)

One very conservative way of looking at it is to look at the maximum of this statistic across stocks. This tells you the “weakest” link in your portfolio formation.

The max statistic is the right one to look at if you are unwilling to deviate from your “wish portfolio”.

But the “wish portfolio” does not take into account transaction costs

How can portfolios take into account trading costs to reduce total costs substantially?

Can we change the portfolios to reduce trading costs without altering them significantly?

One simple way of looking at this is to look at the 95/75/50 percentiles of the used volume distribution.

If it declines steeply it might make sense to avoid the 5% to 25% of the stocks that are least liquid in you portfolio

But as you deviate from the original portfolio you will have tracking error relative to the original strategy.

crsp=pd.read_pickle('https://github.com/amoreira2/Fin418/blob/main/assets/data/crspm2005_2020.pkl?raw=true')

from pandas.tseries.offsets import *

# change variable format to int

crsp[['permno']]=crsp[['permno']].astype(int)

# Line up date to be end of month

crsp['date']=crsp['date']+MonthEnd(0)

# calculate market equity

# why do we use absolute value of price?

crsp['me']=crsp['prc'].abs()*crsp['shrout']

# drop price and shareoustandng since we won't need it anymore

crsp=crsp[['permno','date','ret', 'me','vol','prc']].sort_values(['permno','date']).set_index('date').drop_duplicates().reset_index()

crsp

| date | permno | ret | me | vol | prc | |

|---|---|---|---|---|---|---|

| 0 | 2005-01-31 | 10001 | -0.040580 | 1.717890e+04 | 515.0 | 6.620000 |

| 1 | 2005-02-28 | 10001 | -0.045166 | 1.642828e+04 | 726.0 | 6.321000 |

| 2 | 2005-03-31 | 10001 | 0.124822 | 1.866375e+04 | 4107.0 | 7.110000 |

| 3 | 2005-04-30 | 10001 | -0.074684 | 1.726987e+04 | 527.0 | 6.579000 |

| 4 | 2005-05-31 | 10001 | 0.219030 | 2.105250e+04 | 1990.0 | 8.020000 |

| ... | ... | ... | ... | ... | ... | ... |

| 763616 | 2020-08-31 | 93436 | 0.741452 | 4.643391e+08 | 4051970.0 | 498.320007 |

| 763617 | 2020-09-30 | 93436 | -0.139087 | 4.067015e+08 | 17331954.0 | 429.010010 |

| 763618 | 2020-10-31 | 93436 | -0.095499 | 3.678235e+08 | 8330610.0 | 388.040009 |

| 763619 | 2020-11-30 | 93436 | 0.462736 | 5.380286e+08 | 7811501.0 | 567.599976 |

| 763620 | 2020-12-31 | 93436 | 0.243252 | 6.689053e+08 | 11962716.0 | 705.669983 |

763621 rows × 6 columns

# data=crsp_m.copy()

# ngroups=10

def momreturns_w(data, ngroups):

# step1. create a temporary crsp dataset

_tmp_crsp = data[['permno','date','ret', 'me','vol','prc']].sort_values(['permno','date']).set_index('date').drop_duplicates()

_tmp_crsp['volume']=_tmp_crsp['vol']*_tmp_crsp['prc'].abs()*100/1e6 # in million dollars like me

# step 2: construct the signal

_tmp_crsp['grossret']=_tmp_crsp['ret']+1

_tmp_cumret=_tmp_crsp.groupby('permno')['grossret'].rolling(window=12).apply(np.prod, raw=True)-1

_tmp_cumret=_tmp_cumret.reset_index().rename(columns={'grossret':'cumret'})

_tmp = pd.merge(_tmp_crsp.reset_index(), _tmp_cumret[['permno','date','cumret']], how='left', on=['permno','date'])

# merge the 12 month return signal back to the original database

_tmp['mom']=_tmp.groupby('permno')['cumret'].shift(2)

# step 3: rank assets by signal

mom=_tmp.sort_values(['date','permno']) # sort by date and firm identifier

mom=mom.dropna(subset=['mom'], how='any')# drop the row if any of these variables 'mom','ret','me' are missing

mom['mom_group']=mom.groupby(['date'])['mom'].transform(lambda x: pd.qcut(x, ngroups, labels=False,duplicates='drop'))

# create `ngroups` groups each month. Assign membership accroding to the stock ranking in the distribution of trading signal

# in a given month

# transform in string the group names

mom=mom.dropna(subset=['mom_group'], how='any')# drop the row if any of 'mom_group' is missing

mom['mom_group']=mom['mom_group'].astype(int).astype(str).apply(lambda x: 'm{}'.format(x))

mom['date']=mom['date']+MonthEnd(0) #shift all the date to end of the month

mom=mom.sort_values(['permno','date']) # resort

# step 4: form portfolio weights

def wavg_wght(group, ret_name, weight_name):

d = group[ret_name]

w = group[weight_name]

try:

group['Wght']=(w) / w.sum()

return group[['permno','Wght']]

except ZeroDivisionError:

return np.nan

# We now simply have to use the above function to construct the portfolio

# the code below applies the function in each date,mom_group group,

# so it applies the function to each of these subgroups of the data set,

# so it retursn one time-series for each mom_group, as it average the returns of

# all the firms in a given group in a given date

weights = mom.groupby(['date','mom_group']).apply(wavg_wght, 'ret','me')

# merge back

weights=mom.merge(weights,on=['date','permno'])

weights=weights.sort_values(['date','permno'])

weights['mom_group_lead']=weights.groupby('permno').mom_group.shift(-1)

weights['Wght_lead']=weights.groupby('permno').Wght.shift(-1)

weights=weights.sort_values(['permno','date'])

def wavg_ret(group, ret_name, weight_name):

d = group[ret_name]

w = group[weight_name]

try:

return (d * w).sum() / w.sum()

except ZeroDivisionError:

return np.nan

port_vwret = weights.groupby(['date','mom_group']).apply(wavg_ret, 'ret','Wght')

port_vwret = port_vwret.reset_index().rename(columns={0:'port_vwret'})# give a name to the new time-seires

weights=weights.merge(port_vwret,how='left',on=['date','mom_group'])

port_vwret=port_vwret.set_index(['date','mom_group']) # set indexes

port_vwret=port_vwret.unstack(level=-1) # unstack so we have in each column the different portfolios, and in each

port_vwret=port_vwret.port_vwret

return port_vwret, weights

port_ret, wght=momreturns_w(crsp, 10)

C:\Users\alan.moreira\AppData\Local\Temp\ipykernel_1440\3351365901.py:48: DeprecationWarning: DataFrameGroupBy.apply operated on the grouping columns. This behavior is deprecated, and in a future version of pandas the grouping columns will be excluded from the operation. Either pass `include_groups=False` to exclude the groupings or explicitly select the grouping columns after groupby to silence this warning.

weights = mom.groupby(['date','mom_group']).apply(wavg_wght, 'ret','me')

---------------------------------------------------------------------------

ValueError Traceback (most recent call last)

Input In [4], in <cell line: 1>()

----> 1 port_ret, wght=momreturns_w(crsp, 10)

Input In [3], in momreturns_w(data, ngroups)

48 weights = mom.groupby(['date','mom_group']).apply(wavg_wght, 'ret','me')

50 # merge back

---> 51 weights=mom.merge(weights,on=['date','permno'])

52 weights=weights.sort_values(['date','permno'])

54 weights['mom_group_lead']=weights.groupby('permno').mom_group.shift(-1)

File ~\AppData\Roaming\Python\Python39\site-packages\pandas\core\frame.py:10819, in DataFrame.merge(self, right, how, on, left_on, right_on, left_index, right_index, sort, suffixes, copy, indicator, validate)

10800 @Substitution("")

10801 @Appender(_merge_doc, indents=2)

10802 def merge(

(...)

10815 validate: MergeValidate | None = None,

10816 ) -> DataFrame:

10817 from pandas.core.reshape.merge import merge

> 10819 return merge(

10820 self,

10821 right,

10822 how=how,

10823 on=on,

10824 left_on=left_on,

10825 right_on=right_on,

10826 left_index=left_index,

10827 right_index=right_index,

10828 sort=sort,

10829 suffixes=suffixes,

10830 copy=copy,

10831 indicator=indicator,

10832 validate=validate,

10833 )

File ~\AppData\Roaming\Python\Python39\site-packages\pandas\core\reshape\merge.py:170, in merge(left, right, how, on, left_on, right_on, left_index, right_index, sort, suffixes, copy, indicator, validate)

155 return _cross_merge(

156 left_df,

157 right_df,

(...)

167 copy=copy,

168 )

169 else:

--> 170 op = _MergeOperation(

171 left_df,

172 right_df,

173 how=how,

174 on=on,

175 left_on=left_on,

176 right_on=right_on,

177 left_index=left_index,

178 right_index=right_index,

179 sort=sort,

180 suffixes=suffixes,

181 indicator=indicator,

182 validate=validate,

183 )

184 return op.get_result(copy=copy)

File ~\AppData\Roaming\Python\Python39\site-packages\pandas\core\reshape\merge.py:794, in _MergeOperation.__init__(self, left, right, how, on, left_on, right_on, left_index, right_index, sort, suffixes, indicator, validate)

784 raise MergeError(msg)

786 self.left_on, self.right_on = self._validate_left_right_on(left_on, right_on)

788 (

789 self.left_join_keys,

790 self.right_join_keys,

791 self.join_names,

792 left_drop,

793 right_drop,

--> 794 ) = self._get_merge_keys()

796 if left_drop:

797 self.left = self.left._drop_labels_or_levels(left_drop)

File ~\AppData\Roaming\Python\Python39\site-packages\pandas\core\reshape\merge.py:1297, in _MergeOperation._get_merge_keys(self)

1295 rk = cast(Hashable, rk)

1296 if rk is not None:

-> 1297 right_keys.append(right._get_label_or_level_values(rk))

1298 else:

1299 # work-around for merge_asof(right_index=True)

1300 right_keys.append(right.index._values)

File ~\AppData\Roaming\Python\Python39\site-packages\pandas\core\generic.py:1905, in NDFrame._get_label_or_level_values(self, key, axis)

1902 other_axes = [ax for ax in range(self._AXIS_LEN) if ax != axis]

1904 if self._is_label_reference(key, axis=axis):

-> 1905 self._check_label_or_level_ambiguity(key, axis=axis)

1906 values = self.xs(key, axis=other_axes[0])._values

1907 elif self._is_level_reference(key, axis=axis):

File ~\AppData\Roaming\Python\Python39\site-packages\pandas\core\generic.py:1867, in NDFrame._check_label_or_level_ambiguity(self, key, axis)

1859 label_article, label_type = (

1860 ("a", "column") if axis_int == 0 else ("an", "index")

1861 )

1863 msg = (

1864 f"'{key}' is both {level_article} {level_type} level and "

1865 f"{label_article} {label_type} label, which is ambiguous."

1866 )

-> 1867 raise ValueError(msg)

ValueError: 'date' is both an index level and a column label, which is ambiguous.

wght.head()

| date | permno | ret | me | vol | prc | volume | grossret | cumret | mom | mom_group | Wght | mom_group_lead | Wght_lead | port_vwret | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2006-02-28 | 10001 | -0.010537 | 27522.091006 | 439.0 | 9.390 | 0.412221 | 0.989463 | 0.499266 | 0.411365 | m8 | 0.000016 | m8 | 0.000024 | -0.003999 |

| 1 | 2006-03-31 | 10001 | 0.170394 | 32222.679329 | 777.0 | 10.990 | 0.853923 | 1.170394 | 0.560008 | 0.446795 | m8 | 0.000024 | m8 | 0.000020 | 0.032930 |

| 2 | 2006-04-30 | 10001 | -0.094631 | 29173.399441 | 883.0 | 9.950 | 0.878585 | 0.905369 | 0.526377 | 0.499266 | m8 | 0.000020 | m8 | 0.000024 | 0.018943 |

| 3 | 2006-05-31 | 10001 | -0.010452 | 28633.911396 | 319.0 | 9.766 | 0.311535 | 0.989548 | 0.239037 | 0.560008 | m8 | 0.000024 | m7 | 0.000023 | -0.046612 |

| 4 | 2006-06-30 | 10001 | -0.076387 | 26464.681343 | 1186.0 | 9.020 | 1.069772 | 0.923613 | 0.014145 | 0.526377 | m7 | 0.000023 | m6 | 0.000017 | 0.001877 |

# construct dollars of each stock that need to be bought (sold) at date t+1

mom=wght.copy()

mom['trade']=(mom.Wght_lead*(mom.mom_group==mom.mom_group_lead)-mom.Wght*(1+mom.ret)/(1+mom.port_vwret))

mom['trade_newbuys']=(~(mom.mom_group==mom.mom_group_lead))*mom.Wght_lead

# per dollar of position how much do you have to trade every month?

mom.groupby(['date','mom_group']).trade.apply(lambda x:x.abs().sum()).loc[:,'m9'].plot()

mom.groupby(['date','mom_group_lead']).trade_newbuys.apply(lambda x:x.abs().sum()).loc[:,'m9'].plot()

<AxesSubplot:xlabel='date'>

total_trade=mom.groupby(['date','mom_group']).trade.apply(lambda x:x.abs().sum()).loc[:,'m9']+mom.groupby(['date','mom_group_lead']).trade_newbuys.apply(lambda x:x.abs().sum()).loc[:,'m9']

total_trade.plot()

<AxesSubplot:xlabel='date'>

# lets look at the most illiquid stocks, the stocks that I will likely have most trouble trading

# lets start by normalizing the amount of trade per stock volume

mom['tradepervol']=mom.trade/mom.volume

mom['trade_newbuyspervol']=mom.trade_newbuys/mom.volume

# this allow us to study how much of the volume of each stock I will be "using"

# lets choose a position size, here in millions of dollars , because that is the normalization we used for the volume data

Position=1e3 #(1e3 means one billion dollars)

threshold=0.05

(Position*(mom.groupby(['date','mom_group']).tradepervol.quantile(threshold).loc[:,'m9'])).plot()

(Position*(mom.groupby(['date','mom_group']).tradepervol.quantile(1-threshold).loc[:,'m9'])).plot()

(Position*(mom.groupby(['date','mom_group']).trade_newbuyspervol.quantile(1-threshold).loc[:,'m9'])).plot()

<AxesSubplot:xlabel='date'>

Tracking error

Let $\(W^{wishportfolio}_t\)\( and \)\(W^{Implementationportfolio}_t\)$ weights , then consider the following regression

a good implementation portfolio has \(\beta=1\) and \(\sigma(\epsilon)\) and \(\alpha\approx 0\).

So one can think of \(|\beta-1|\), \(\sigma(\epsilon)\) , and \(\alpha\) as three dimensions of tracking error.

The \(\beta\) dimension can be more easily correted by levering up and down the tracking portoflio (of possible)

The \(\sigma(\epsilon)\) can only be corrected by simply making the implemenetation portoflio more similar to the wish portfolio. The cost of this is not obvious. Really depends how this tracking error relates to other stuff in your portfolio.

\(\alpha\) is the important part. The actual cost that you expect to pay to deviate from the wish portfolio

In the industry people typicall refer to tracking error as simply

The volatility of a portfolio that goes long the implementation portfolio and shorts the wish portfolio.

This mixes together \(|\beta-1|\), \(\sigma(\epsilon)\) and completely ignores \(\alpha\)

In the end the Implementation portfolio is chosen by trading off trading costs (market impact) and opportunity cost (tracking error).

So you can simply construct strategies that avoid these 5% less liquid stocks, and see how much your tracking error increases and whether these tracking errors are worth the reduction in trading costs

How to construct an Implementation portfolio?

A simple strategy: weight by trading volume -> this make sure that you use the same amount of trading volume across all your positions

Harder to implement: do not buy stocks that are illiquid now or likely to be illiquid next period. Amounts to add another signal interected to the momentum signal. Only buy if illiquid signal not too strong.

How to change our code to implement the volume-weighted approach?

def momreturns(data, ngroups,wghtvar='me'):

# step1. create a temporary crsp dataset

_tmp_crsp = data[['permno','date','ret', 'me','vol','prc']].sort_values(['permno','date']).set_index('date').drop_duplicates()

_tmp_crsp['volume']=_tmp_crsp['vol']*_tmp_crsp['prc'].abs()*100/1e6 # in million dollars like me

# step 2: construct the signal

_tmp_crsp['grossret']=_tmp_crsp['ret']+1

_tmp_cumret=_tmp_crsp.groupby('permno')['grossret'].rolling(window=12).apply(np.prod, raw=True)-1

_tmp_cumret=_tmp_cumret.reset_index().rename(columns={'grossret':'cumret'})

_tmp = pd.merge(_tmp_crsp.reset_index(), _tmp_cumret[['permno','date','cumret']], how='left', on=['permno','date'])

# merge the 12 month return signal back to the original database

_tmp['mom']=_tmp.groupby('permno')['cumret'].shift(2)

# step 3: rank assets by signal

mom=_tmp.sort_values(['date','permno']) # sort by date and firm identifier

mom=mom.dropna(subset=['mom'], how='any')# drop the row if any of these variables 'mom','ret','me' are missing

mom['mom_group']=mom.groupby(['date'])['mom'].transform(lambda x: pd.qcut(x, ngroups, labels=False,duplicates='drop'))

# create `ngroups` groups each month. Assign membership accroding to the stock ranking in the distribution of trading signal

# in a given month

# transform in string the group names

mom=mom.dropna(subset=['mom_group'], how='any')# drop the row if any of 'mom_group' is missing

mom['mom_group']=mom['mom_group'].astype(int).astype(str).apply(lambda x: 'm{}'.format(x))

mom['date']=mom['date']+MonthEnd(0) #shift all the date to end of the month

mom=mom.sort_values(['permno','date']) # resort

# step 4: form portfolio weights

def wavg_wght(group, ret_name, weight_name):

d = group[ret_name]

w = group[weight_name]

try:

group['Wght']=(w) / w.sum()

return group[['permno','Wght']]

except ZeroDivisionError:

return np.nan

# We now simply have to use the above function to construct the portfolio

# the code below applies the function in each date,mom_group group,

# so it applies the function to each of these subgroups of the data set,

# so it retursn one time-series for each mom_group, as it average the returns of

# all the firms in a given group in a given date

weights = mom.groupby(['date','mom_group']).apply(wavg_wght, 'ret',wghtvar)

# merge back

weights=mom.merge(weights,on=['date','permno'])

weights=weights.sort_values(['date','permno'])

weights['mom_group_lead']=weights.groupby('permno').mom_group.shift(-1)

weights['Wght_lead']=weights.groupby('permno').Wght.shift(-1)

weights=weights.sort_values(['permno','date'])

def wavg_ret(group, ret_name, weight_name):

d = group[ret_name]

w = group[weight_name]

try:

return (d * w).sum() / w.sum()

except ZeroDivisionError:

return np.nan

port_vwret = weights.groupby(['date','mom_group']).apply(wavg_ret, 'ret','Wght')

port_vwret = port_vwret.reset_index().rename(columns={0:'port_vwret'})# give a name to the new time-seires

weights=weights.merge(port_vwret,how='left',on=['date','mom_group'])

port_vwret=port_vwret.set_index(['date','mom_group']) # set indexes

port_vwret=port_vwret.unstack(level=-1) # unstack so we have in each column the different portfolios, and in each

port_vwret=port_vwret.port_vwret

return port_vwret, weights

momportfoliosme,wght=momreturns(crsp,10,wghtvar='me')

momportfoliosvol,wght_vol=momreturns(crsp,10,wghtvar='vol')

momportfolios=momportfoliosme.merge(momportfoliosvol,left_index=True,right_index=True,suffixes=['_me','_vol'])

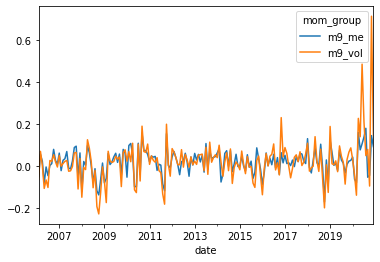

momportfolios[['m9_me','m9_vol']].plot()

<AxesSubplot:xlabel='date'>

Is this good how do you compare?

Look at tracking error

Don’t be fooled by the long-only performance–replciating the market is easy!

# lets look at it's tracking error

y=momportfolios['m9_vol']

x=momportfolios['m9_me']

x=sm.add_constant(x)

results = sm.OLS(y,x).fit()

results.summary()

| Dep. Variable: | m9_vol | R-squared: | 0.611 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.609 |

| Method: | Least Squares | F-statistic: | 277.7 |

| Date: | Wed, 01 May 2024 | Prob (F-statistic): | 4.18e-38 |

| Time: | 17:39:33 | Log-Likelihood: | 242.81 |

| No. Observations: | 179 | AIC: | -481.6 |

| Df Residuals: | 177 | BIC: | -475.2 |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | -0.0050 | 0.005 | -1.020 | 0.309 | -0.015 | 0.005 |

| m9_me | 1.3036 | 0.078 | 16.664 | 0.000 | 1.149 | 1.458 |

| Omnibus: | 207.284 | Durbin-Watson: | 1.986 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 8869.659 |

| Skew: | 4.469 | Prob(JB): | 0.00 |

| Kurtosis: | 36.307 | Cond. No. | 16.7 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Observations:

The beta difference can be adjusted by taking a smaller position on the implementation portfolio

The alpha is the actual tracking error loss. How much you expect to loose.

One calculation that people do is to see how much you are getting for your momentum exposure

[momportfolios['m9_vol'].mean()/results.params[1]*12,momportfolios['m9_me'].mean()*12]

[0.17998714127139948, 0.2261181726535535]

But be careful to not over interpret this. We are working today with a very short sample, less than 20 years, for average returns tests that is not much at all.

But beta/residulas are well measured even in fairly short samples.

In addition to that you also have to eat the strategy residual risk

[results.resid.std(),momportfolios['m9_me'].std()]

[0.06249878812223737, 0.06005053427493518]

It is sizable, about the level of the original strategy volatility

How our implemented strategy compare with the desired strategy?

df=pd.read_pickle('https://raw.githubusercontent.com/amoreira2/Fin418/main/assets/data/df_WarrenBAndCathieW_monthly.pkl')

Factors=df.drop(['BRK','ARKK','RF'],axis=1)

Factors = Factors.rename(columns={Factors.columns[-1]: 'Mom'})

Factors.mean()*12

Mkt-RF 0.100955

SMB 0.012654

HML 0.011914

RMW 0.041875

CMA 0.012701

Mom 0.069910

dtype: float64

portfolios=momportfolios.merge(Factors,left_index=True,right_index=True)

portfolios.head()

| m0_me | m1_me | m2_me | m3_me | m4_me | m5_me | m6_me | m7_me | m8_me | m9_me | ... | m6_vol | m7_vol | m8_vol | m9_vol | Mkt-RF | SMB | HML | RMW | CMA | Mom | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2006-02-28 | -0.012354 | -0.006109 | 0.012724 | 0.017131 | 0.012390 | 0.014931 | 0.008770 | 0.008683 | -0.003999 | -0.051872 | ... | 0.016308 | 0.012868 | -0.016740 | -0.064788 | -0.0030 | -0.0042 | -0.0034 | -0.0051 | 0.0191 | -0.0184 |

| 2006-03-31 | 0.043584 | 0.029708 | 0.034453 | 0.012203 | 0.013299 | 0.005424 | 0.014716 | 0.026616 | 0.032930 | 0.054823 | ... | 0.023306 | 0.102972 | 0.149737 | 0.069339 | 0.0146 | 0.0338 | 0.0060 | 0.0006 | -0.0041 | 0.0126 |

| 2006-05-31 | -0.026365 | -0.024219 | 0.001555 | -0.015647 | -0.030534 | -0.027217 | -0.032916 | -0.031146 | -0.046612 | -0.080706 | ... | -0.058780 | -0.056930 | -0.079337 | -0.107404 | -0.0357 | -0.0285 | 0.0241 | 0.0115 | 0.0146 | -0.0370 |

| 2006-06-30 | -0.029358 | 0.006137 | -0.002789 | 0.002618 | 0.004338 | 0.002428 | 0.011803 | 0.001877 | 0.023077 | -0.005062 | ... | -0.019315 | -0.004445 | 0.013017 | -0.067229 | -0.0035 | -0.0024 | 0.0085 | 0.0132 | -0.0007 | 0.0154 |

| 2006-07-31 | -0.058296 | -0.036734 | 0.022658 | -0.005353 | 0.024988 | 0.010822 | 0.005927 | -0.008269 | -0.022406 | -0.046551 | ... | -0.008441 | -0.033398 | -0.040144 | -0.102966 | -0.0078 | -0.0363 | 0.0260 | 0.0163 | 0.0090 | -0.0212 |

5 rows × 26 columns

# things to look at:

#y=portfolios['m9_me']

#y=momportfolios['m9_vol']

#y=momportfolios['m9_me']-momportfolios['m0_me']

y=portfolios['m9_me']-portfolios['m0_me']

x=portfolios['Mom']

x=sm.add_constant(x)

results = sm.OLS(y,x).fit()

results.summary()

| Dep. Variable: | y | R-squared: | 0.645 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.643 |

| Method: | Least Squares | F-statistic: | 227.5 |

| Date: | Wed, 01 May 2024 | Prob (F-statistic): | 6.34e-30 |

| Time: | 17:46:46 | Log-Likelihood: | 150.75 |

| No. Observations: | 127 | AIC: | -297.5 |

| Df Residuals: | 125 | BIC: | -291.8 |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| const | -0.0231 | 0.007 | -3.504 | 0.001 | -0.036 | -0.010 |

| Mom | 1.9579 | 0.130 | 15.085 | 0.000 | 1.701 | 2.215 |

| Omnibus: | 93.627 | Durbin-Watson: | 2.091 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 691.904 |

| Skew: | -2.555 | Prob(JB): | 5.69e-151 |

| Kurtosis: | 13.229 | Cond. No. | 19.7 |

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

why such a large difference even for the strategy that follows the Momentum strategy?